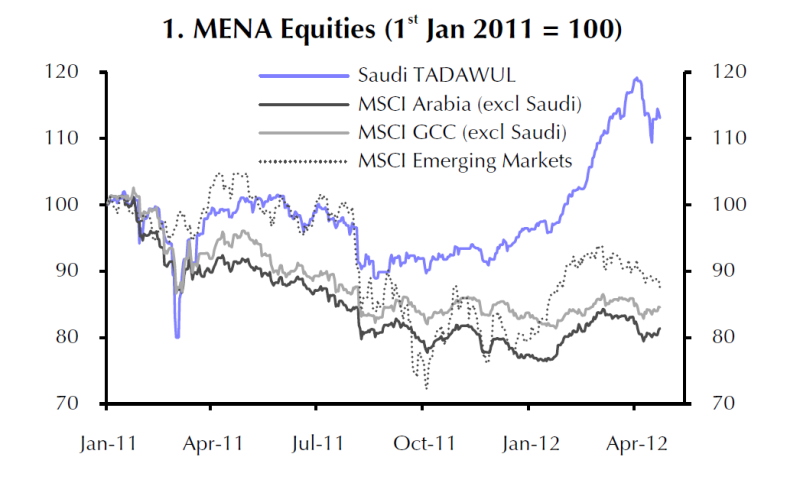

Analysts are sharply divided over the outcome of Egypt’s torturous negotiations with the IMF over a $3.2bn loan after the country’s parliament rejected an austerity plan, heaping on the risk of a current account crisis. The move came despite comments by the IMF this Saturday that multilateral lenders will “soon” make good on their commitment to provide $20bn of loans to shore up Arab transition economies - initially pledged in May 2011 - and after mass protests in Egypt this weekend ended peacefully, seen as a sign of emerging political stability. Economic conditions in the countries hit by the Arab Spring have generally worsened since multilateral discussions commenced in June last year and the majority of the Arab world’s equity markets continue to underperform compared to other emerging markets. In the case of Egypt, the largest economy in the region, any agreement to disburse $20bn of funding to Egypt and Tunisia would need tacit IMF approval, said analysts.

However, on Tuesday, the Egyptian parliament overwhelmingly rejected the army-appointed cabinet's plan to slash state spending, triggering fears that political leaders will fail to impose politically-sensitive fiscal austerity plans in order to secure an IMF agreement.

A deal with the global policy lender was suspended last year as leaders in Egypt predicted the economic situation would improve. But economic conditions in the countries hit by the Arab Spring have generally deteriorated and the majority of the Arab world’s equity markets continue to underperform compared to other emerging markets. A current account crisis looms, without urgent redress, said analysts. “The country might be forced to accept IMF conditions less favourable than before because they are continually finding it harder to straighten out their balance of payments,” says Said Hirsh, Middle East economist at Capital Economics, a macroeconomic research consultancy in London.

And “a deeper economic crisis – which Egypt is on route for – might act as a catalyst for change and a rush by Egypt to accept IMF conditions,” says Hirsh. “But this is not likely to happen in the next month or so."

But another well-connected MENA analyst argued the IMF deal is likely finally to reach fruition, despite the political posturing. “All sides that are part of this agreement are waiting for IMF approval which will happen in the next two weeks. Once this happens, all other loan offers will fall into place,” says the analyst. “Indeed, the pending presidential election will add to political stability and hopefully encourage all parties involved to come to agreement over an acceptable fiscal package.”

Political infighting between the Muslim Brotherhood and the ruling military has played a part in a delayed IMF agreement. “Although the IMF must take the lead in negotiations, to date Egypt has been reluctant to accept any conditions as leadership there is concerned about being perceived as weak if a government in transition accepts stringent IMF conditions,” says Hirsh.

Even with an IMF agreement, Hirsh at Capital Economics calculates Egypt’s external financing needs for the year stands at around $11bn.

Medium-term outlook

Nevertheless, analysts are confident over the region’s medium to long term economic performance.

“Growth potential in the region is huge,” says Hirsh. “The region is starting from a relatively low point and international funds will come on the condition of fiscal and institutional reform. As fiscal and institutional reform continues, confidence in these countries will grow. Foreign and domestic investment as well as capital inflows will swell. It’s only a matter of time before this happens,” he says.

In Egypt, the banking system lives on lending to the government and about 40% of banking assets are in treasury yields. “For banks, it is less risky and more profitable to lend to the government right now,” explains Hirsh. “But at the same time, funds are limited for the private sector.”

| Source: Capital Economics |