Research from ANZ shows that since the collapse of Lehman Brothers in October 2008, AUDUSD has rallied by 35 big figures in London and New York time zones, but fallen by 30 big figures in Asia. That means the surge in AUDUSD from $0.6 to parity and beyond has been fuelled offshore.

| AUDUSD by time zones - cumulative change since October 2008 |

|

| Source: Bloomberg, ANZ |

The obvious answer to the underperformance of AUD in Asia is the presence of Australian importers in that time zone, along with Reserve Bank of Australia (RBA). The central bank, acting as an agent of the Australian government, executes the majority of its FX transactions in its local time zone, most of which are sales.

However, the volumes of AUD traded in Australia, which the RBA put at a daily average of $46 billion in April, are dwarfed by those of other centres with access to different time zones.

In Singapore, which enjoys access to early London trading, average daily trading volumes in AUD stood at $32.1 billion in April, according to the Monetary Authority of Singapore.

Meanwhile, Bank of England figures put the daily average of AUD traded in April at $144.2 billion in London, while the Federal Reserve of New York reported daily volumes of $47.4 billion.

That increased liquidity on offer in London and New York attracts larger FX players, who have been consistent buyers of AUD in recent years.

Principal among those have been the world’s reserve managers, who have been building up their stockpiles in AUD as they diversify into Australian government paper.

Indeed, the RBA, which has recently provided information showing that up to 23 central banks hold AUD in reserve portfolios, has singled out the Swiss National Bank as a buyer of AUD, as it looks to diversify away from the euros it receives as a consequence of maintaining the SFr1.20 floor in EURCHF.

However, a look at the more recent moves in AUDUSD suggests that the Australian currency’s much heralded link to equities is on the wane. During the summer, the greatest gains in AUDUSD have come in the London time zone, despite the strong performance of US equities as the Federal Reserve hinted at, and then enacted, QE3.

“It suggests that the rally in US equity markets, to which many commentators attribute the AUD’s strength, and on which many participants focus as a barometer of risk, may not be as important for the AUD prospects as previously thought,” says Andrew Salter, FX strategist at ANZ.

| Time zone effect in 2012 - cumulative chnage since March 1, 2012 |

|

| Source: Bloomberg, ANZ |

The conclusion might be simply that investors should look to lighten long AUDUSD positions during the currency’s local session and vice versa.

However, that is to assume that sovereign demand for Australian government paper will, or indeed can, persist.

Gavin Friend, strategist at National Australia Bank, says after aggressive buying of AUD in recent years, central banks might be getting close to their benchmark holdings of Australian paper.

“If marginal sovereign buyers are getting saturated, demand for AUD should start to wane,” he says.

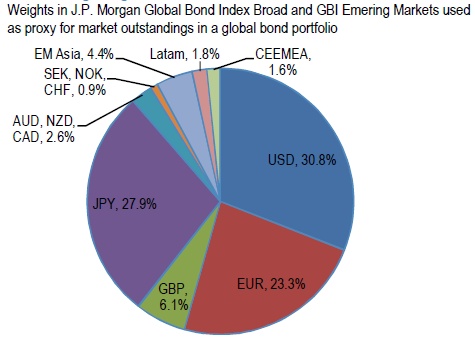

Indeed, according to JPMorgan, based on market outstandings of global government bonds, reserve managers’ currency allocation to leading commodity currencies – AUD, NZD and CAD – should be about 2.5% and is at benchmark.

| Benchmark in a reserve portfolio weighted by market |

|

| Source: JPMorgan |

Furthermore, with foreign holdings of Australian government debt close to 80%, there is a shortage of paper available to buy.

That is a supply problem unlikely to be solved by the Australian government, which is committed to balancing its budget and which is expected to issue only between $15 billion to $20 billion in long-term debt next year.

Reserve managers could always move along the risk curve and buy lesser-quality Australian paper. However, if not, that would imply the global pattern in the AUDUSD might be nearing an end.

And it might not just affect the AUD. Other currencies that have benefited from the AAA status of their government paper amid the recent market turmoil – CAD, NZD, SEK and NOK for instance – might also find that reserve manager demand is on the wane and therefore buying pressure during the London time zone is dissipating.