Just as Eskimos are said to have a large number of words to describe ‘snow’, financial language might soon generate multiple phrases to describe the fine regulatory art of “negative unintended consequences”.

As any student of complex systems – or fans of Back to the Future – will tell you, small shifts in individual inputs can trigger system-level changes – often negative. In finance, this lesson rings painfully true, as 2008 highlighted erroneous regulatory assumptions on liquidity, credit-quality, and counterparty risk.

Fast-forward to the eurozone crisis: regulatory assumptions that AAA-rated bonds were risk-free served to trigger a negative sovereign-bank feedback loop, knocking global growth. In other words, well-intentioned dictums to target micro-level behaviour can trigger large-scale macro consequences.

For all the populist fervor then about perceived policy inaction to address systemic risk, many banks see it differently: investor flight from banks’ equity and bond products has taken root over the years, amid fears that new rules will render business models uneconomic.

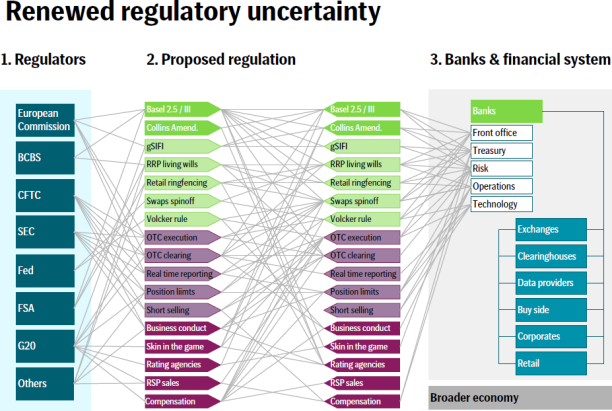

The following chart highlights how bankers and risk managers are struggling to breathe while the global financial landscape gets redrawn, assuming a shape many regulators will admit, off-the-record, is unclear, four years after the ground-breaking G20 London summit.

|

| Source: Oliver Wyman, SEB |

Whether it’s rules on swaps, shadow banks, funding markets, counterparty exposures, many analysts, not just on the right, fear regulators are perpetuating their own concentration of risk through one-size-fits-all rules.

While Basel regulators say they seek to reduce arbitrage risk and reckon convergence of capital standards will boost market transparency, those agitating for some diversity in the business models of banks and financial intermediaries are losing the battle, though the opportunity costs are unclear.

On a final note, some reckon operational risk has overtaken credit risk for banks, relegating growth as a priority. As Alastair Ryan, then banks analyst at UBS in London, told Euromoney last year, operational risk is at all-time high.

“Changes in regulations, changes in what other stakeholders consider to be acceptable, the risk that the behaviours of certain employees become associated with the institution as a whole – those are indeed much more expensive for banks these days than credit [risk],” he says.

There is a lot more to say about this chart, including the rise of shadow banking, supervisory fragmentation and the surge in compliance costs for banks. For more on evolving debates in financial regulation, go here.