by Jamie Grant, Global Head of Rates & Credit FRC, Financial & Risk,

Thomson Reuters

|

Reuters/Stefan Wermuth |

The OTC derivatives market has seen several defaults in the past two decades, each of which has led to a rethink of industry practices. Nowhere is this more evident than in the evaluation of counterparty credit risk, with processes that are now unrecognizable from those of the 1980s and 1990s, when this type of risk wasn’t even factored into swap pricing.

Regulatory pressures

Managing credit exposure is particularly challenging given the demands from US and European regulators for buy-side central clearing, increased customer protection and bilateral swap margining.

Complex requirements from the Basel Committee on Banking Supervision for Credit Valuation Adjustments (CVA) are among the factors not only driving up the costs of compliance but focusing financial institutions on the most efficient ways to deploy capital.

Collateralization, or the margining of bilateral or cleared derivatives positions, could be a major expense. Get it wrong and you can tie up hundreds of millions of dollars in cash or collateral that could be more effectively deployed elsewhere in the bank.

In addition to the demands of the Dodd-Frank Act and Basel III, there are new reporting and accounting standards including EMIR, MiFID, IFRS9 and IFRS13 and FAS. Together these regulations present a massive amount of complexity that compounds operational risk in the market.

This regulatory entanglement is making it harder for banks to focus on more profitable aspects of their businesses, and exacerbates the need for sharp, decisive and well-informed decision-making, not least about how best to measure and monitor counterparty credit risk on an on-going basis.

The complexity

The impact of these challenges is not isolated to a particular back office or compliance function. Rather, it spans the entire marketplace, including rates sales and structuring desks, corporate treasuries, auditors and risk consultancies.

While all market participants face the same environment, for each the challenges are subtly different. From the Basel III capital charge, to calculating the CVA of a large portfolio; from complying with IFRS9 Hedge Accounting requirements to managing CSA collateral arrangements – firms must find an intelligent solution to its unique set of requirements.

In fact, the complexity of the challenge is one of the biggest issues facing the industry. For example, while CVA has been around for years it is only more recently that is has been recognized as an issue for derivatives users.

Counterparty risk must be managed at the portfolio level, not solely the deal level, so a new trade could increase the counterparty risk with one counterparty, but reduce it with another. When combined with the new regulatory requirement for this tool, there is a pressing need for a practical solution.

What’s needed

Many of the larger banks have the resources for measuring CVA, but this is not the case for most buy-side firms and corporate treasury departments. A home-grown solution is not cheap and is almost unattainable for smaller firms, given the requirement to knit together a robust and complete entity database, along with a raft of issuer and sector credit curves.

Regardless of the approach – whether built or managed in-house, or by using a service such as Thomson Reuters Eikon – firms need to ensure that they are covered in three core areas: at the system level; for swap pricing; and for portfolio-level analytics.

This is particularly important as the impact of credit and collateral requirements has to be viewed holistically, to take advantages of efficiencies such as margin off-setting and compression.

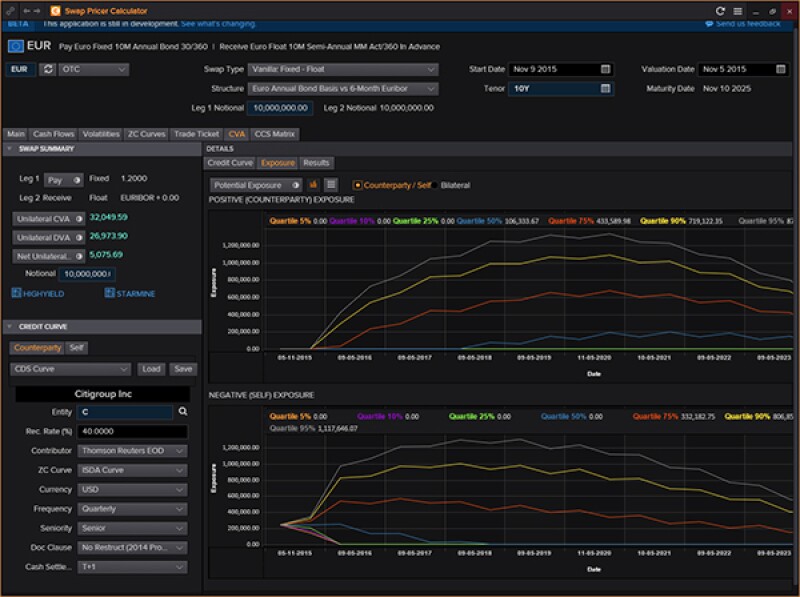

|

Swap Price Calculator in Thomson Reuters Eikon supports discovery of optimum funding currency and cross asset CVA using American Monte Carlo Engine |

Integrated pricing and analytics

From the system perspective, it is important to have multi-asset pricing, valuation and reporting capabilities. Pricing and analytics should be integrated and available across all portfolios, including CVA across assets.

Firms need access to collateral management including different types of collateral and Credit Support Annexes (CSA). In addition, a robust system should deliver mark-to-market reporting, P&L management, counterparty management, time-bucketed interest-rate risk and interest-rate historical VaR.

Swap pricing

Market data remains an integral component of counterparty credit risk management. Unlike in years past, the quality and transparency of price information to the buy side has improved sharply – especially for vanilla contracts.

However, there is still a strong demand for accurate pricing across the curve, and for more exotic products, such as swaptions, cancellable contracts, inflation swaps and other hard-to-price contracts.

Ideally, a swap-pricing calculator should have the ability to set the type of collateral (including cash) and ISDA/CSA details (haircuts, thresholds, etc) for each counterparty and allow the user to create leg-by-leg custom swaps.

Portfolio-level analysis

Buy-side firms and corporate treasurers need to create, share and manage portfolios of interest-rate derivatives, cash bonds, bond futures, repo and interbank lending. It’s also important to be able to calculate the portfolio P&L and mark-to-market using real-time data or conduct valuations for an historical date.

A multi-currency system that lets you organize positions in multiple ways should let you conduct scenario analysis on the portfolio. Of course, it must provide you full collateral management capabilities, including CSA and Standard CSA, and portfolio CVA including incremental CVA, as well as hedge accounting.

The compliance burden for participants is only likely to increase in the years ahead and while a professional system for managing counterparty credit risk will be invaluable, there will still be a need for resources to remain fully compliant with all regulations.

While it is easy to paint all regulation as a burden, the new ecosystem that is emerging for derivatives actually promises a brighter future for participants. There will be a higher level of price and model transparency, a wider and more competitive range of execution platforms (swap execution facilities), more efficient central clearing options (such as compression in all its flavours and cross-product margining) and, most importantly, a deeper understanding of all risks that relate to derivatives contracts.

This can only be good for the long-term health of the derivatives markets.

Jamie Grant manages the global proposition for Rates & Credit Fixed Income at Thomson Reuters. Prior to Thomson Reuters, Jamie held senior positions within government bond and derivatives trading, over a 15 year career in international debt capital markets.