Balancing the Books

IFRS 16 and Aviation Finance

The most recent projections published by The International Air Transport Association (IATA) suggests the global airline industry net profit will rise from the $34.5 billion expected in 2017 to a forecast figure of $38.4 billion in 2018. The boost in net profit is being fuelled by robust demand, reduced finance costs and operational efficiencies, and will translate to the fourth consecutive year of sustainable profits for the airline industry.

The positive macro fundamentals underpinning the airline industry growth have also benefitted the aviation finance industry. Lessors have experienced strong demand for narrow body jets by both airlines and investors, and new-order delivery lags suggest that there is no sign of such demand abating in the near-term.

That said, lessor optimism emanating from the forecast profit projections and strong macro demographics has been tempered by the challenges which the industry faces.

The profitability outlined above has improved the airline industry’s credit profile, which, together with increased liquidity and investor appetite, has contributed to lease rate compression in recent periods, impacting lessor margins.

The recent airline struggles of Air Berlin, Alitalia, Monarch, and VIM have provided a timely reminder of industry fragilities. International and US tax reform, cost pressures from infrastructure, labour and potentially fuel, and competitive pressures provide further headaches.

And finally, IFRS 16 Leases is just around the corner (effective for annual periods beginning on or after 1 January 2019), which the industry consensus suggests will have a notable impact from both an operational, reporting, and implementation perspective.

The path to issuance of IFRS 16 has been long and winding, initially being added to the IASB’s agenda in July 2006.

But what does IFRS 16 hold in store for the aviation finance industry? It is clear that the impact on airlines is far more pronounced than their financing partners. Substantial new assets and liabilities will appear on airline balance sheets, while reported profit and performance measures will be impacted.

Perhaps most significantly, the impact on individual airlines will depend on their particular financing and leasing structures, and may be very different from the impact on their peers.

It is less clear how the market will approach the key judgement areas in the standard such as the discount rate assumption which may have the largest quantitative impact on the lease asset and liability valuations, and how the market will perceive, and respond to, the anticipated impacts.

To provide perspective on the market sentiment, Deloitte and Euromoney Institutional Investor Thought Leadership have teamed up to prepare this report on the impact of IFRS 16 on the aviation finance industry.

The report contains perspectives gleaned from 381 senior executives surveyed from the aviation finance industry as well as in-depth interviews conducted with senior industry executives and independent experts. It provides fascinating insight on the operational, financial and implementation challenges which the standard presents.

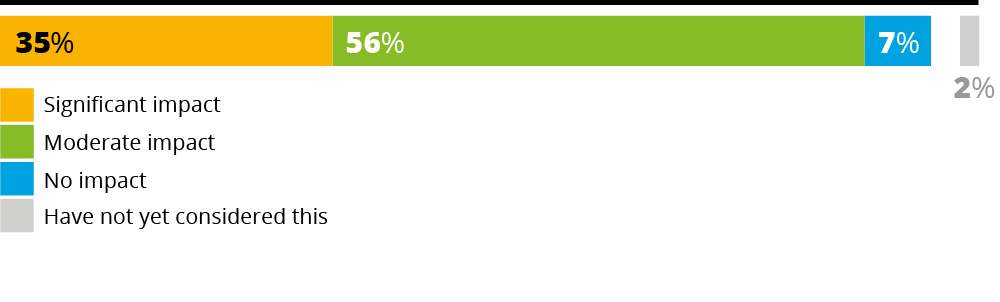

Respondents suggest that the influence of IFRS 16 will extend far beyond financial reporting concerns, with 59% of airlines believing the standard will have a significant impact on their business.

I expect that professionals and stakeholders in the aviation finance industry will find this work insightful at a time when the industry is charting its course through the adoption of this new reporting framework.

The introduction of the new accounting standard IFRS 16 will reshape the balance sheets of most companies that rent valuable equipment. Airlines will be particularly affected once the international standard takes effect from January 2019, and preparations are well underway for the new reporting challenges.

However, the impact of IFRS 16 could extend beyond accounting and into the commercial decisions of airlines, lessors and financiers. By forcing airlines to recognise lease payments as liabilities, IFRS 16 threatens to change their approach to fleet planning, or to how they structure their leases.

Euromoney Institutional Investor Thought Leadership has worked with Deloitte to examine the impact and likelihood of these changes, and what they mean for different stakeholders, with particular attention paid to the often contrasting views of airlines and lessors.

Drawing on a worldwide survey of 381 senior executives involved in the sector, as well as in-depth interviews with nine experts at leading airlines, lessors and financiers, its key findings are:

Most airlines (59%) believe IFRS 16 will have a significant impact on their business. Understandably, airlines that rely heavily on leased aircraft are more likely to predict this.

Among airlines’ top concerns are transitional arrangements, the review of existing lease and finance data, and renegotiation of lease contracts.

The bulk of the rest of the industry expects only a moderate impact. This is unsurprising, given that IFRS 16 principally overhauls accounting for lessees, not lessors, only 38% of which think that IFRS 16 will seriously affect their business.

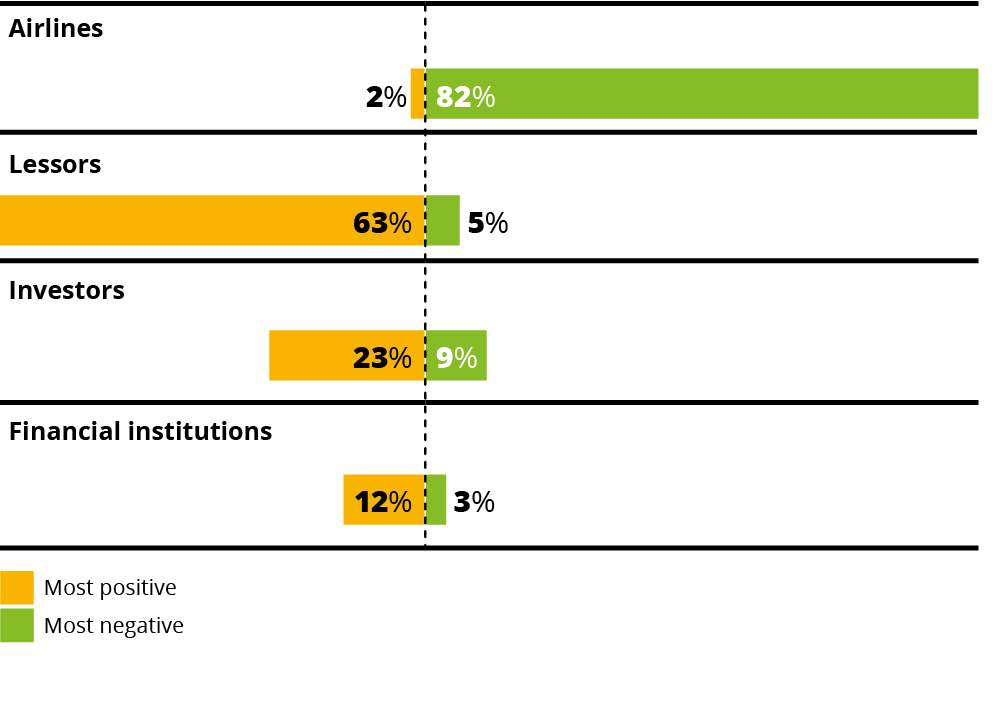

A related finding is that 82% of respondents expect IFRS 16 to be more negative for airlines than for lessors, investors or financial institutions.

Lease contracts are expected to change in the wake of IFRS 16. Airlines (90%) and lessors (74%) say they will need to renegotiate existing leases as well as create new standard terms.

Industry experts interviewed for this report say lease durations could become shorter as airlines seek to reduce liabilities and minimise IFRS 16’s impact on leverage ratios. Respondents agreed, highlighting lease tenors and lease rates above other factors likely to change in lease contracts.

Some lessors interviewed for this report, however, promise to resist any changes to lease contracts – a potential source of tension with airlines in the wake of IFRS 16.

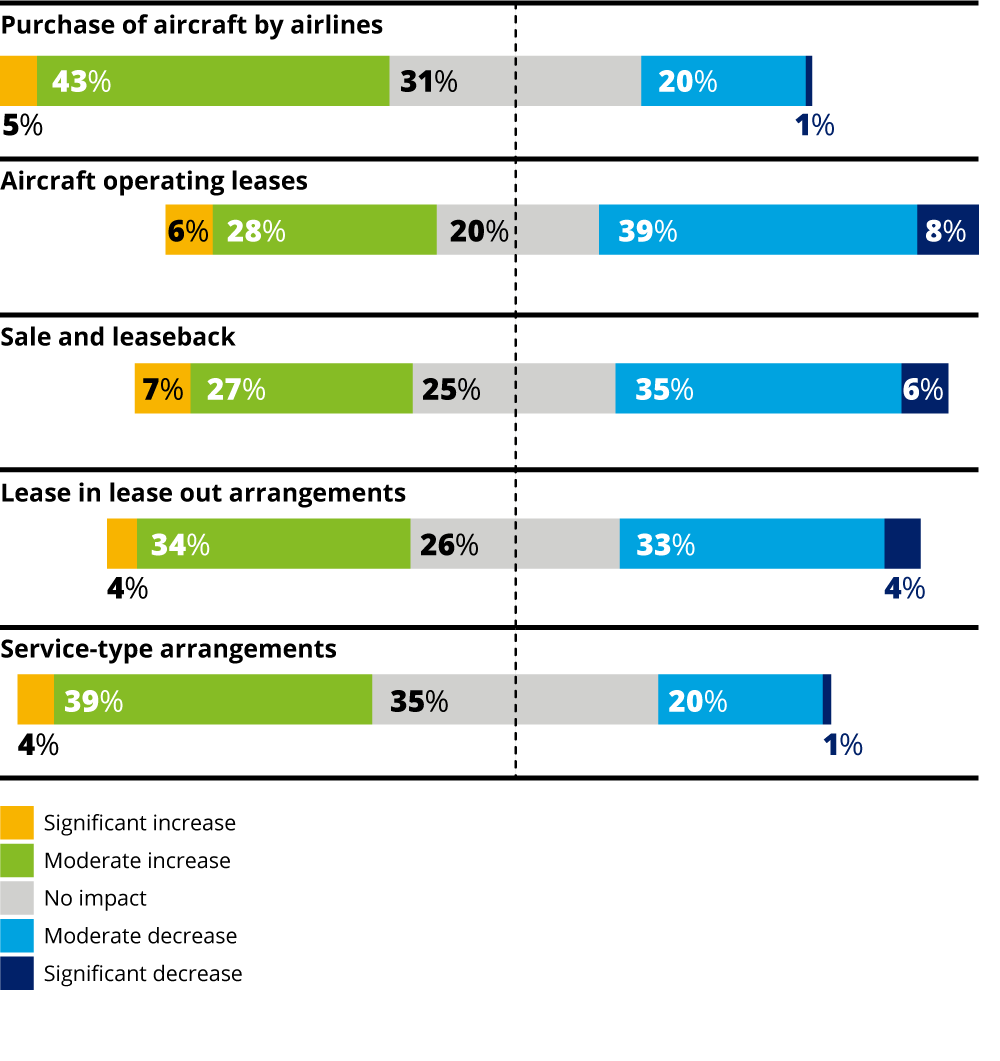

There are mixed views on the impact of IFRS 16 on leasing volumes. While a significant number of survey respondents predict that operating lease and sale-leaseback volumes will fall in light of the new accounting standard, most expect no change or even an increase in leasing activity.

However, opinion is weakly held and varies according to stakeholder. Airlines are as likely to predict a rise as a fall in operating leasing after IFRS 16, while lessors veer more towards a fall. Lessor interviewees, in contrast, appear sure that the advantages of leasing will override any concerns about its accounting treatment.

Taken together, 44% of respondents think that IFRS 16 will herald a decline in sale-leaseback or operating lease deals.

This aligns roughly with the 48% of respondents who say that IFRS 16 will prompt airlines to purchase more aircraft themselves.

IFRS 16’s impact on gearing ratios could be particularly problematic. While the new accounting will alter a host of key performance metrics, 63% of the wider aviation finance industry and, in particular, 69% of airlines are most concerned by changes to leverage ratios.

Airlines worry this might breach debt covenants, or increase borrowing costs. Almost half of survey respondents, including 61% of lessors, think that IFRS 16 raises the risk of covenant violations by airlines.

Financiers interviewed for this report counter that most covenants already account for the impact of operating leases on debt, although they concede it will be time-consuming to ensure this is the case.

Whatever the impact, there is broad agreement about the complexity of re-negotiating finance and lease contracts. A third of airlines and 23% of lessors say this will be very challenging, while most of the rest predict some difficulties in doing so.

Currency volatility under IFRS 16 accounting is a concern for airlines, particularly those that lease more heavily. Most leases are paid in dollars, but these payments – recognised as liabilities under the new standard – must be converted to the local currency of an airline, pushing additional foreign exchange volatility through its profit and loss statement.

Managing this extra volatility is the most significant challenge of IFRS 16, say a fifth of airlines. Furthermore, currency denomination is among the lease terms most susceptible to change due to IFRS 16, according to those carriers that rely more heavily on leasing.

Introduction

Aircraft leasing has rapidly become an integral part of aviation finance. Operating leases offer low initial capital outlays, simpler risk management and enhanced operational flexibility. These are key advantages for low-cost carriers, which want to scale quickly, but many full-service airlines are also now enthusiastic lessees.

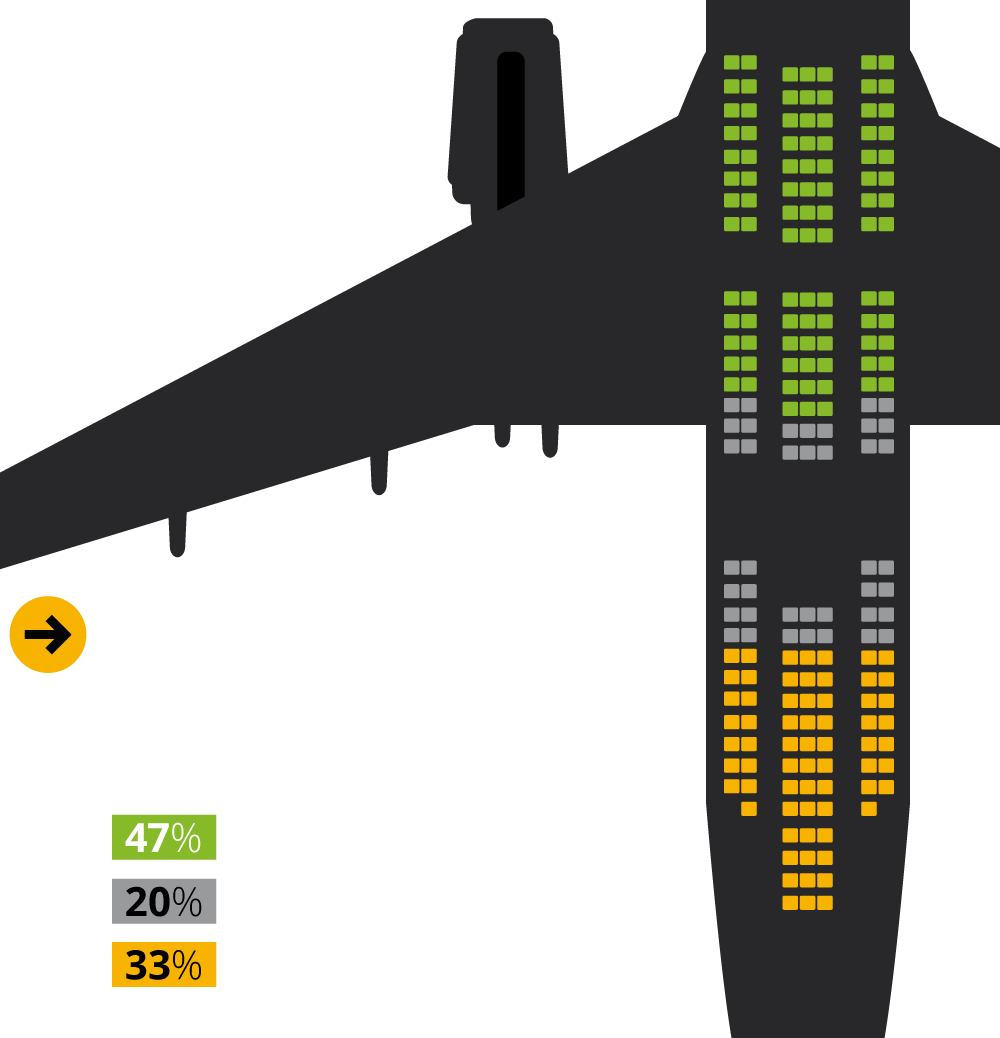

Today, 38% of the global fleet of roughly 26,000 aircraft is leased, according to Airfinance Journal’s Fleet Tracker. If leasing sustains historic growth, that share will reach 50% in the next 10 years.

Long before then – from January 2019 – airlines will have to record operating leases on their balance sheets. Under IFRS 16 this means recognising leased aircraft as right-of-use assets and rental payments as liabilities.

According to Fleet Tracker data, approximately $325 billion of aircraft assets will transfer to airline balance sheets as a result. It comes therefore as no surprise that aviation experts agree that the industry will be affected by IFRS 16.

For this report, we surveyed 381 executives from airlines, lessors, investors and other sector stakeholders globally (see About the survey section for methodology). Of them, 91% predict at least a moderate impact from IFRS 16 on aviation.

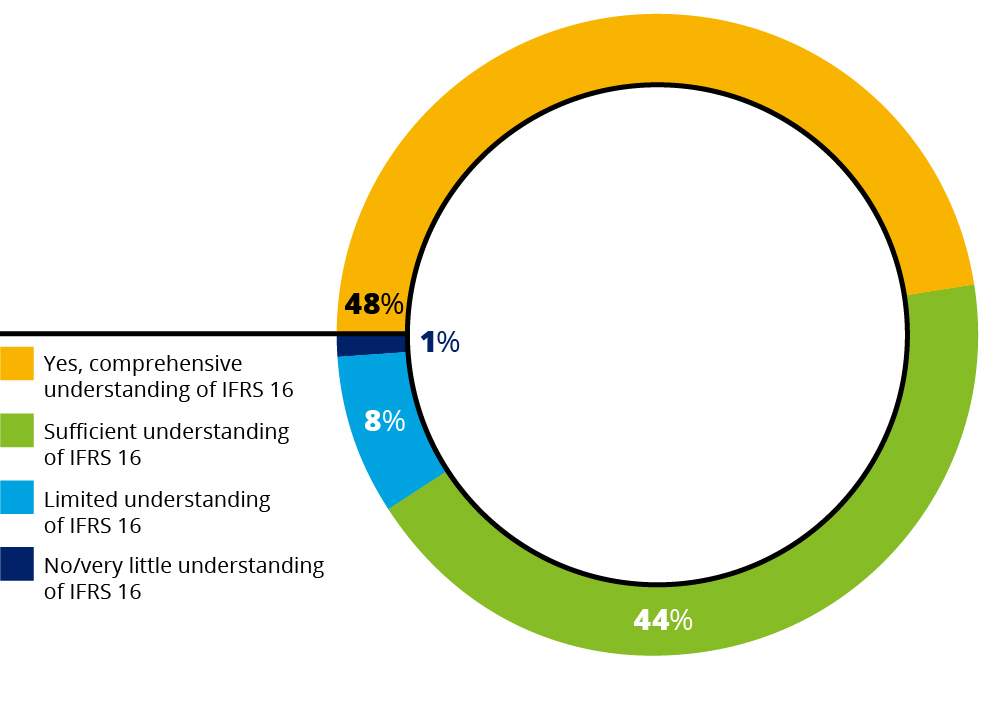

Most airlines feel prepared for this shift, with 90% telling our survey they have sufficient or comprehensive understanding of IFRS 16, confidence that is matched by the wider industry, only 9% of which admit little or no comprehension of the new accounting standard.

Worth noting, though, is a difference in understanding of IFRS 16’s accounting implications and of its operational impact. For while there is broad consensus on how the standard will affect various financial metrics, there is considerably less agreement on how it might influence airlines’ decisions to lease or buy aircraft.

Of course, such choices do not occur in isolation. Oil prices, interest rates and competitive pressures all influence financing plans, and must be weighed up years in advance.

On the accounting side, at least, 74% of respondents feel they have sufficient time to implement IFRS 16.

Tore Østby, CFO, Norwegian

“Discussions have been taking place for years about how to account for leases in the future, and we have anticipated the need to modify the measurement and presentation of the operational leases as a lessee,” says Tore Østby, Chief Financial Officer of Norwegian.

That said, adoption of IFRS 16 is a major bureaucratic task – one that 59% of airlines say will have a significant impact on their business (chart 1), a figure that rises to 66% for airlines that lease more than a quarter of their fleet. Most of the rest predict a moderate impact.

“Applying the new standard should easily be possible for most contracts but some will need some thorough analysis to determine whether they are fully within scope,” says Østby.

As expensive assets, aircraft are firmly within the remit of IFRS 16, although a minority of leases – such as those for less than one year – are treated differently.

Once items relevant to IFRS 16 are identified, airlines like Norwegian must then assess the impact on a host of metrics – such as gearing ratio, EBITDA and return on capital employed – and whether those changes will have knock-on effects – on debt covenants, for instance.

If those effects prove too disruptive, or implementation too cumbersome, some airlines might reduce their use of leased aircraft. Even those that don’t might insist on new lease terms to minimise the impact of IFRS 16, a development that 90% of airlines and 73% of lessors predict (chart 2).

The extent to which airlines alter aircraft procurement due to IFRS 16 also depends on their motivation to lease. For while it’s cheaper to buy than rent in the long run, operating leasing provides flexibility and a route to rapid expansion – advantages that many airlines are unlikely to forego.

It’s also the case that most industry observers already adjust airline debt to include operating lease liabilities, so there is less incentive for airlines to rent fewer aircraft after IFRS 16.

On the other hand, certain airlines value balance sheets with lower debt. One reason for this preference might be the location of the airline or its financier, Marc Bourgade, Chief Executive Officer of Stellwagen Finance, points out: “In some countries local banks are not aviation professionals and do not re-integrate operating leases into the debt.”

To find out how IFRS 16 changes lease accounting, the burden these changes impose and how different stakeholders are likely to respond, Euromoney Institutional Investor Thought Leadership has worked with Deloitte to produce this report. Special attention is reserved for the impact on lease structures and aircraft finance, as well as the contrasting views of airlines and lessors on all of the above issues.

Operational

impact

Perhaps the key question surrounding IFRS 16 is whether its reporting impact could influence commercial decisions. In particular, might it dissuade airlines from leasing aircraft, or make them seek different lease terms?

It’s worth noting that while the industry appears confident in its understanding of IFRS 16’s accounting implications, there is much less consensus about the standard’s operational impact.

Lease or buy?

Almost half of survey respondents believe IFRS 16 will lead to some fall in operating lease deals, but more predict no change or even an increase in activity (chart 3).

Despite such uncertainty, IFRS 16’s impact on operating leasing is “not something we are overly concerned about,” says David Breen, Head of Finance for Dublin-based lessor Avolon.

“Commercial decisions will still be made by airlines in terms of buying or leasing and this change in the accounting treatment should not be a significant component of an airline’s decision,” he adds.

Colm Barrington, CEO, Fly Leasing

Colm Barrington, CEO of Fly Leasing, agrees. By leasing “you are reducing your residual exposure and getting another source of financing as a way to get aircraft quickly – those factors will be more important to airlines than anything IFRS 16 will do to them,” he says.

While more expensive in the long run, operating leasing provides several advantages to finance leases or outright purchases, including flexibility, quicker access to popular aircraft types and lower initial capital outlay. Rapidly expanding operator Norwegian leases almost half its aircraft, and CFO Østby says the airline is “committed to how we finance our fleet”.

Air France-KLM has about 40% of its fleet under operating lease, a ratio it wants to decrease, although that is “not directly linked to IFRS 16,” says Marie-Agnès de Peslouan, Head of Investor Relations for Air France-KLM.

“We do not decide to have aircraft in operating lease because of the accounting treatment,” she says.

Like operating leases, aircraft sold and then rented back by airlines will move onto balance sheets under IFRS 16. In recent years sale-leasebacks have proved a popular choice for airlines seeking liquidity and for new lessors trying to grow their portfolios quickly.

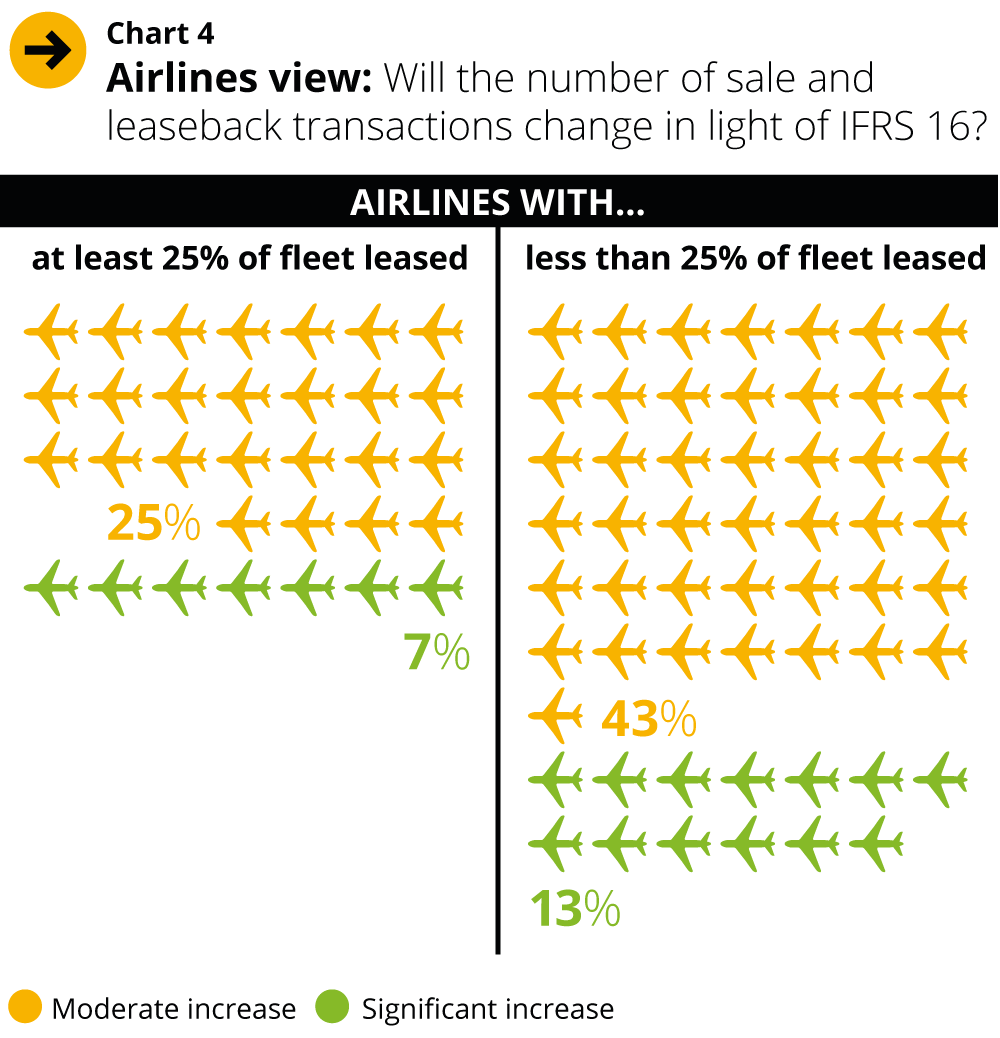

As is the case with operating leases, though, it is hard to predict how IFRS 16 will affect this market: almost as many respondents expect a rise in sale-leasebacks as those who expect a fall.

There’s a clear distinction within those results between airlines that lease less than a quarter of their aircraft and those that lease higher proportions. Not even a third of the latter group expects the sale-leaseback market to continue its rise after IFRS 16, whereas a majority of airlines less reliant on leasing think so (chart 4). This might be because airlines with fewer leases see more capacity for themselves to use the financing option in the future.

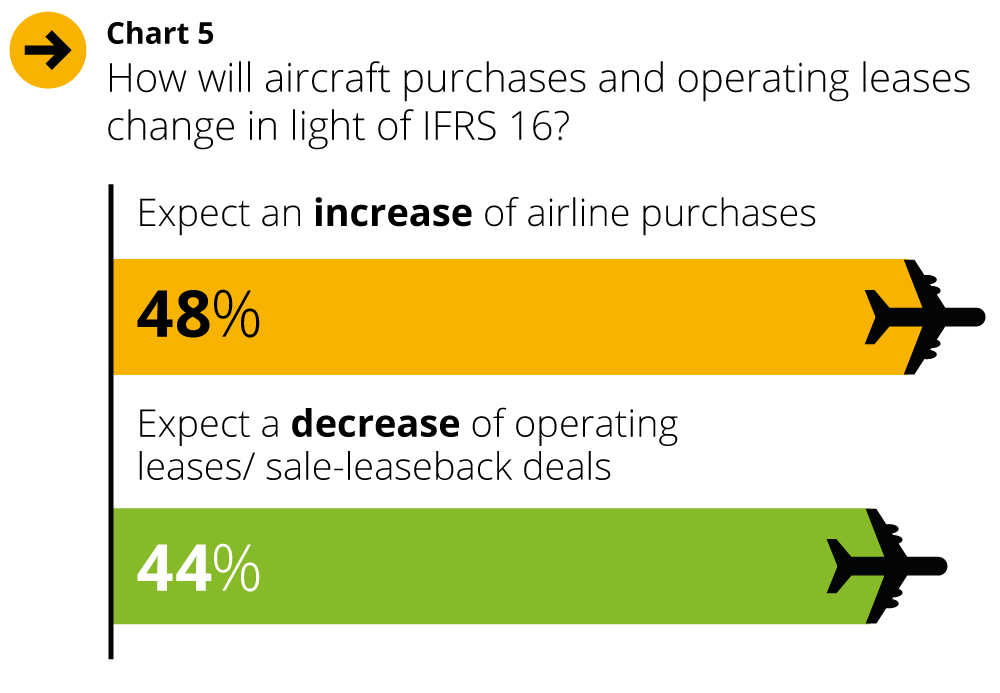

If leasing declines, direct ownership by airlines should rise, and there is a rough correlation between the number of respondents who predict both outcomes: 48% say that aircraft purchases will rise in light of IFRS 16, while 44% think operating lease or sale-leaseback activity will fall (chart 5). Twenty-three percent predict no impact on leases.

“For airlines with sufficient access to liquidity, buying is cheaper than renting in the long term, and they may be more inclined to purchase now that there is no difference from an accounting perspective between operating and finance leases,” says Wui Jin Woon, Head of Aviation, Asia Pacific at Natixis CIB.

Wui Jin Woon, Head of Aviation, Asia Pacific, Natixis CIB

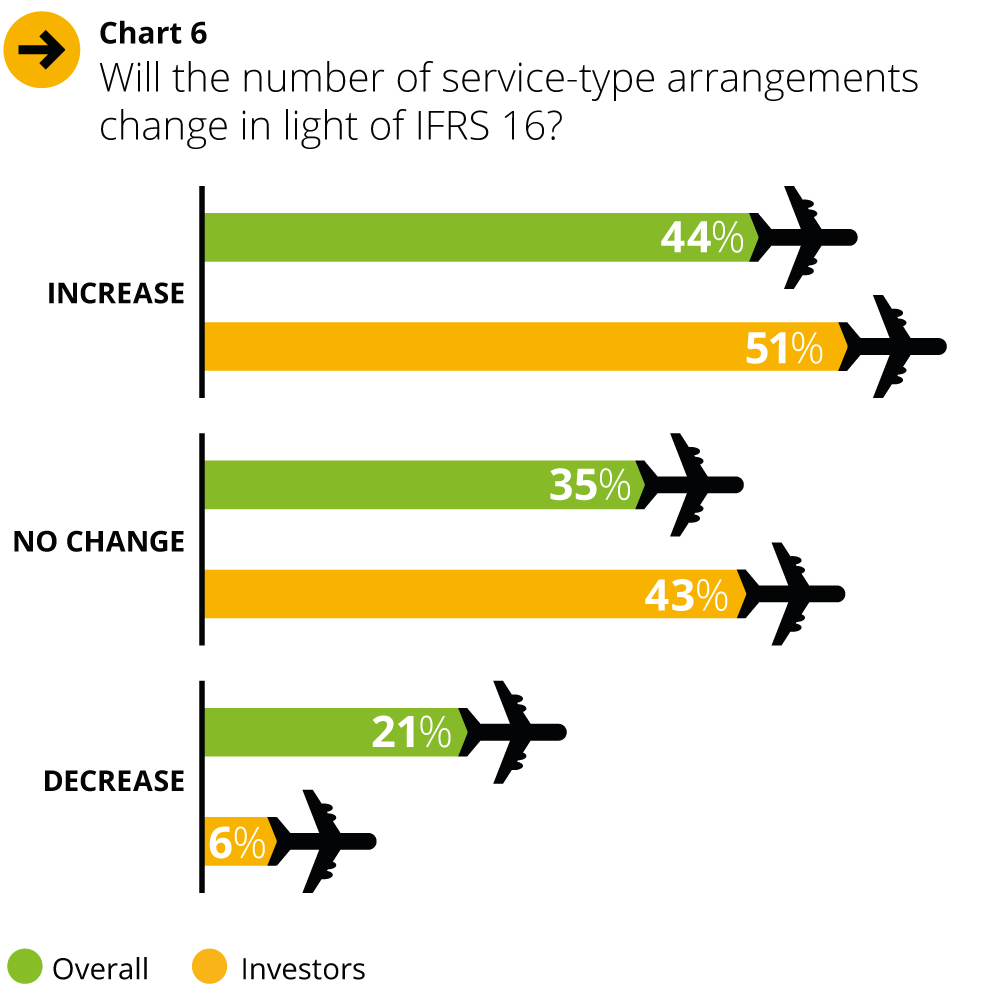

Woon also suggests that IFRS 16 might boost alternative leasing arrangements where airlines pay according to their use of an asset rather than a fixed rate. His view chimes with respondents to our survey from the financing side, 51% of whom predict a rise in service-type arrangements, slightly higher than the 44% figure for the wider survey (chart 6).

There may be some appeal to entering into flexible lease rental arrangements, as any such arrangements which are considered variable payments under IFRS 16 will not appear on the balance sheet.

“It may occur for older aircraft, but we don’t see that becoming the norm for new to medium-life aircraft,” he says. “The fundamentals don’t work for a lessor in terms of stability of cash-flows.”

Restructured leases

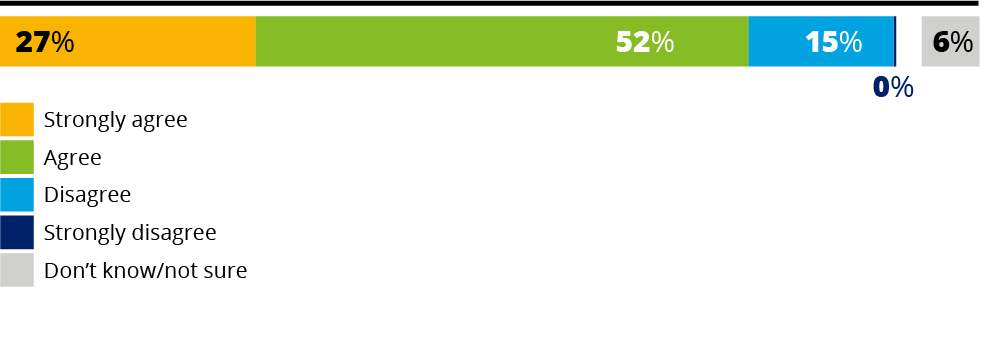

Even if IFRS 16 does not diminish leasing’s appeal, there’s wide agreement that it will influence contract negotiations between airlines and lessors. Existing leases will be renegotiated and new standard terms sought in the future, say 79% of all respondents, 90% of airlines and even 73% of lessors.

“We anticipate that airlines will generally opt for shorter lease terms in order to alleviate the debt burden and gearing ratios, plus we may see certain mechanisms such as extension options be tested with auditors,” says José Abramovici, Global Head of Asset Finance at Crédit Agricole Corporate & Investment Bank.

But David Breen of Avolon warns that lessors – who face extra remarketing costs from shorter leases – would resist this.

“I think airlines will try to push towards shorter terms,” he says, speaking for the world’s third-largest lessor by fleet size. “But I think the core commercial reality of lease rates and lease terms will remain consistent with the supply and demand we currently have in the market.”

These contradicting perspectives might explain why in response to the survey 74% of airlines expect changes to lease tenors, but only 59% of lessors agree (chart 7 below).

That said, Air France-KLM’s de Peslouan expects lessors to be “rather indifferent” to any concessions sought by airlines on the basis of IFRS 16.

In addition, Breen notes there have been no IFRS 16-related requests to modify the contracts of any of Avolon’s almost 600 aircraft under lease.

“We haven’t had conversations with airlines to date about changing terms of the lease contract or adding incentives for shorter leases or breaks within the lease.”

Currency volatility

For airlines outside the United States, under IFRS 16 their lease liabilities will be converted to local currency at each reporting date, giving rise to additional foreign exchange volatility within P&L statements.

As a result, rental currency denominations in lease contracts are likely to change, according to 40% of survey participants.

“From a practical perspective, the ‘real’ foreign exchange risk remains unchanged,” observes Woon. “Nevertheless, for P&L considerations, there may be a preference for lease rental at least partially denominated in domestic currency if lessors and financiers are prepared to consider this.”

In our survey 37% of investors and 19% of airlines flag the management of foreign exchange volatility as the most challenging aspect of IFRS 16 reporting, highlighting that this is more than just an operational issue.

Breen acknowledges that currency “will obviously be a significant concern for certain airlines,” but again predicts resistance to contract amendments from lessors.

“We don’t see a change in terms of the lease negotiations and pulling that FX risk that was already inherent in a lease back to the lessor.”

It is also the case that airlines serving the US can offset volatility with their dollar revenues.

“We have a natural hedge as today we use our revenue in dollars to pay aircraft rent. Tomorrow [post-IFRS 16] we will reimburse the debt with these dollars,” says Séverine Guffroy, who is VP Accounting for Air France-KLM and also Chairwoman of IATA’s accounting working group.

Financing

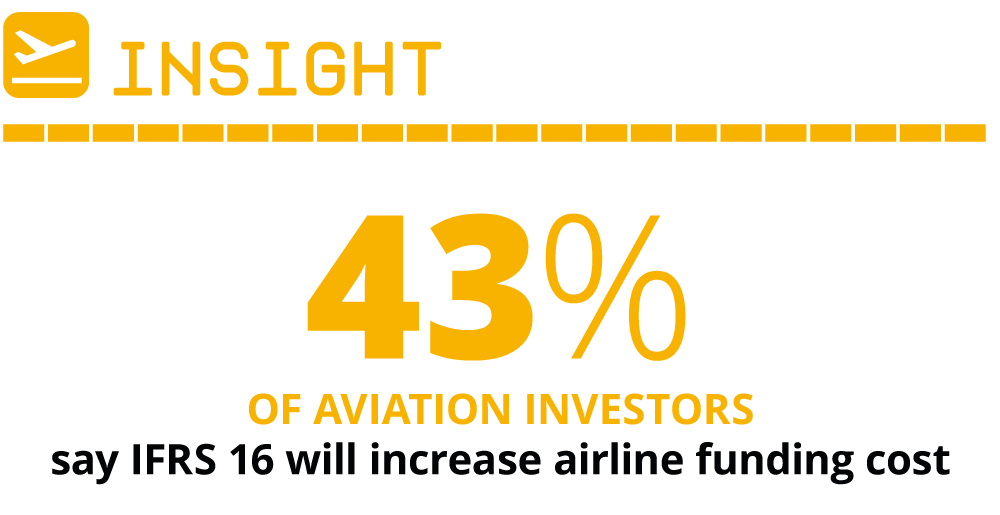

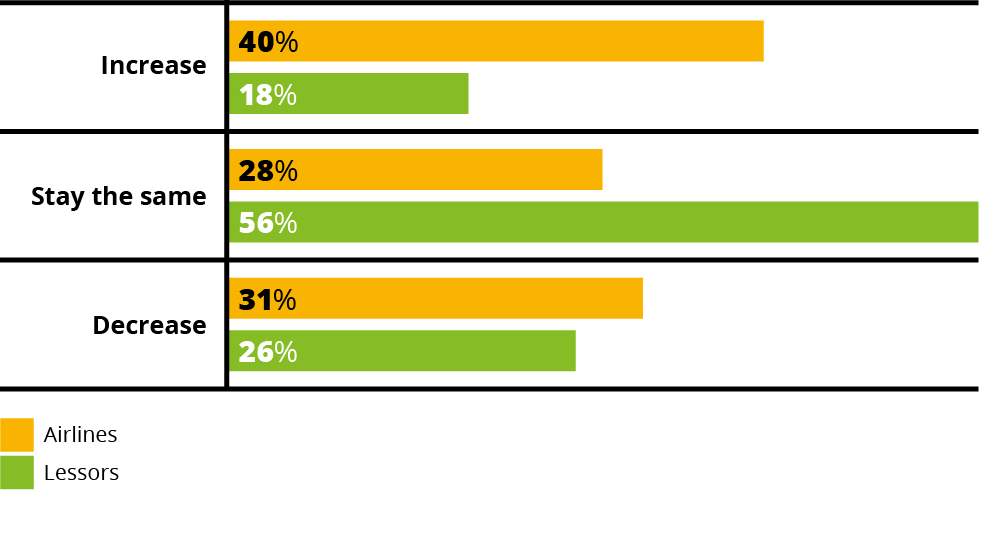

According to our survey, IFRS 16 is much more likely to increase the cost of funding for airlines than for lessors. It’s a view taken across the different segments of the survey, although lessors and investors have a slightly stronger expectation that this will be the case than the airlines themselves.

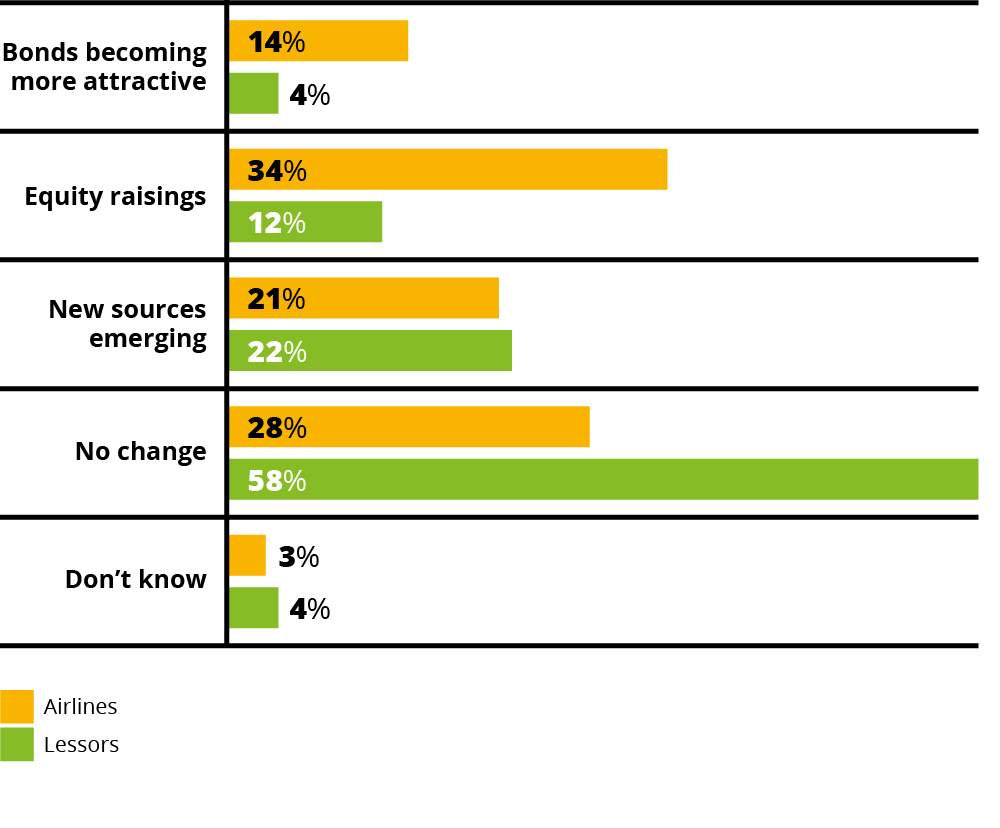

There is less consensus about how IFRS 16 might alter airlines’ fundraising strategies. Overall, one in three expects equity raisings to become more attractive, but smaller minorities also say they expect no change or new sources to emerge, or bonds to become more attractive.

The views are most pronounced among investors, a small majority of whom think equity issues will become more popular (chart 8).

Reporting

impact

Although the consequences of IFRS 16 for fleet planning and finance will take time to materialise, plenty of guidance already exists on how to apply the new standard to various key performance indicators (KPIs).

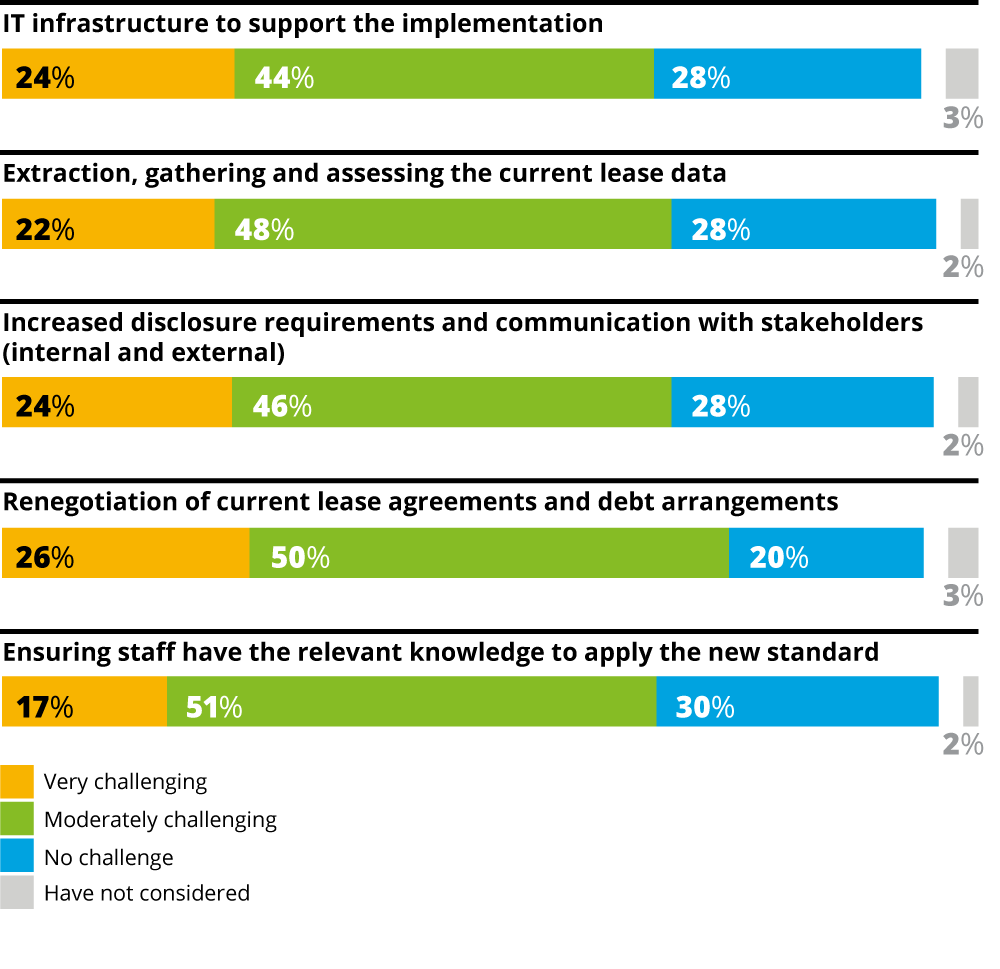

Only a small minority of respondents admit to insufficient understanding of IFRS 16, although almost one in five foresees a big challenge bringing staff up to speed.

Moreover, analysts have long incorporated operating leases into their reading of airline reporting.

“Analysts have been adjusting airlines’ balance sheets for years to capitalise in a proxy for the debt related to leased assets,” says Barry Flannery, Chief Financial Officer of SMBC Aviation Capital.

“Accordingly, it appears that leases offer limited balance sheet benefit for airlines who either borrow in the public markets or deal with specialist financiers,” he adds.

Natixis' Wui Jin Woon concurs: “We currently already take into account and adjust our debt metrics for operating leases in any case, so we expect the impact [of IFRS 16 on analysis] to be minimal.”

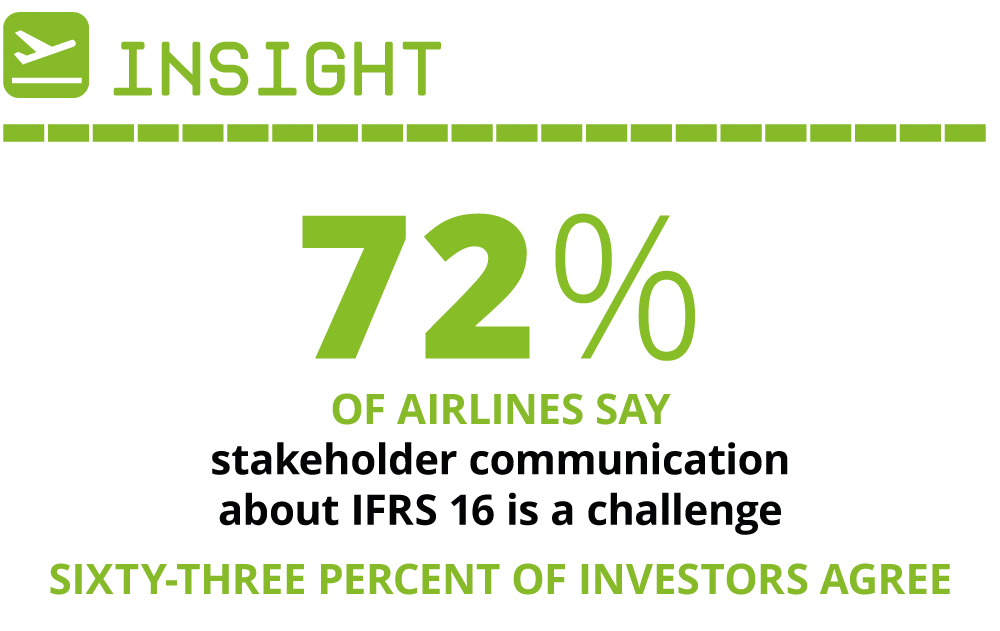

Nevertheless, airlines must ensure clear communication with investors about their accounting methodologies during the transition to IFRS 16. Almost three-quarters of airlines and two-thirds of investors identify this as a challenge.

“For airlines a lot will depend on how they can communicate to financial institutions what the standard is, how it is being implemented and adopted and how the fundamentals of the industry are affected by leasing,” says Breen.

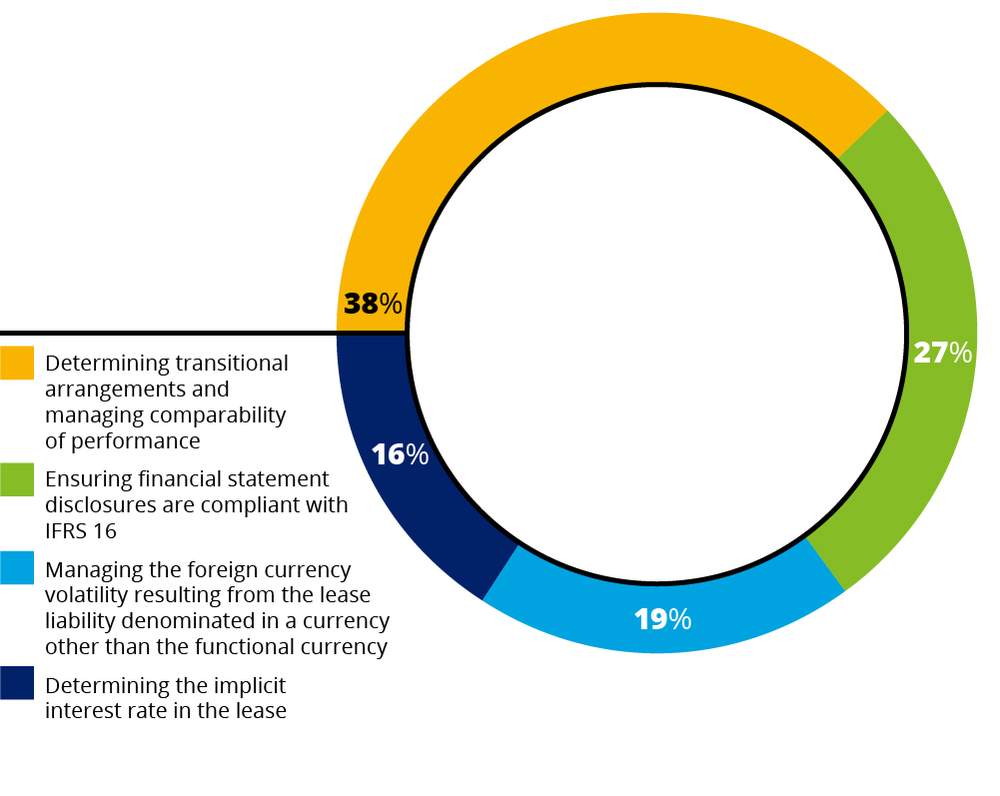

Discount rate

How an airline calculates its discount rate is one of two variables (alongside adoption methodology – discussed in the Implementation section) that it must explain carefully to investors. Essentially, the discount rate applies a present value to future lease payments.

One way to calculate the discount rate is to ascertain the interest rate implicit in a lease, a job that 15% of airlines find the most challenging aspect of IFRS 16 reporting. This is because it requires commercially sensitive information from lessors, which is “not something we will disclose to airlines,” notes Breen.

More airlines aren’t concerned by this because they can use an alternative method: their incremental borrowing rate.

“Only in rare cases will we be able to find the interest rate implicit in the lease,” confirms Norwegian CFO Østby, adding: “In the case of aircraft leases, we will look at interest rates applicable to borrowings associated with our owned aircraft and make any necessary adjustments.”

Since the choice of discount rate affects costs such as depreciation and interest, it will affect numerous financial metrics, changes to which are important to understand for several reasons.

José Abramovici, Global Head of Asset Finance, Crédit Agricole CIB

First, they may affect debt covenants. Second, different analysts use different adjustments, some of which may be further out of line with the new, harmonised standard than others.

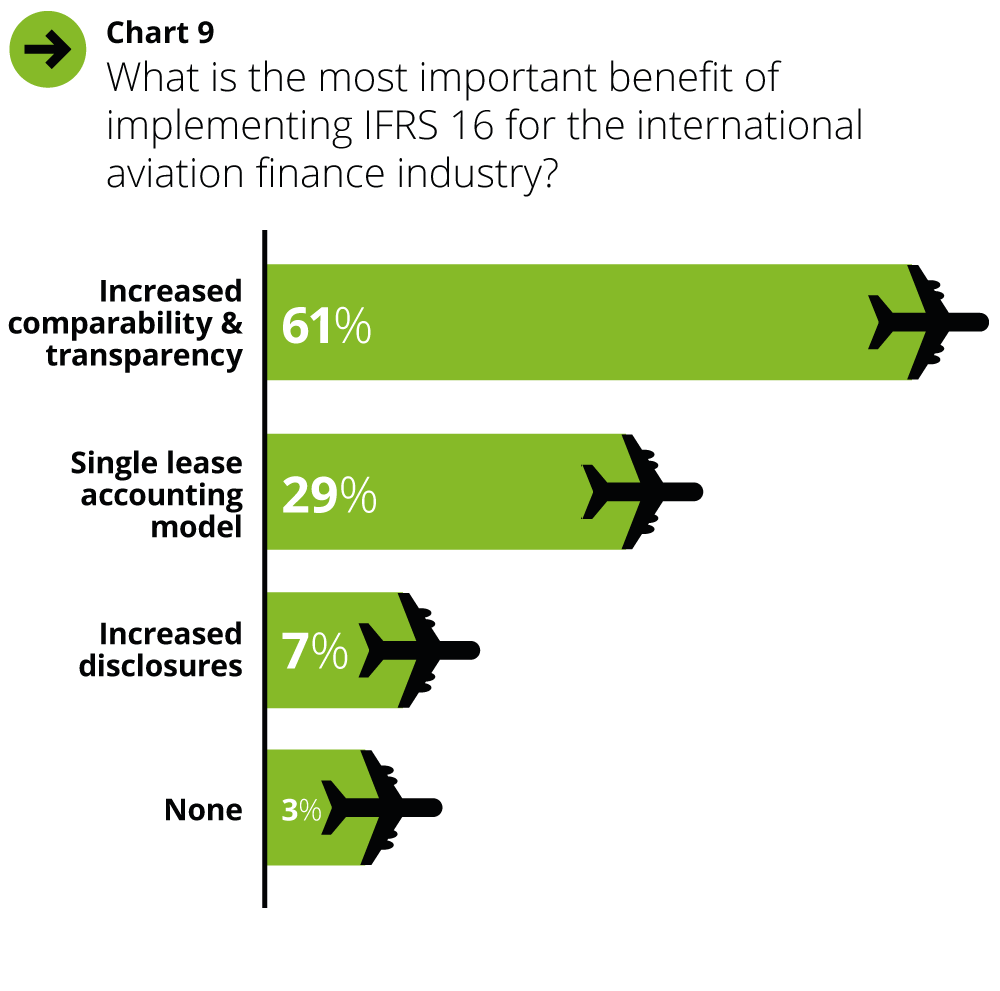

“If implemented correctly, IFRS 16 will increase transparency and provide analysts with more accurate data instead of the output derived from home-made adjustments,” says Abramovici of Crédit Agricole.

Of all survey respondents, 61% pointed at increased transparency and comparability as the main benefit of IFRS 16 (chart 9). However, peer comparison of metrics is complicated by jurisdiction (IFRS and non-IFRS implementing – see Implementation chapter), while historical comparisons are affected by implementation methodology.

Balance sheet changes

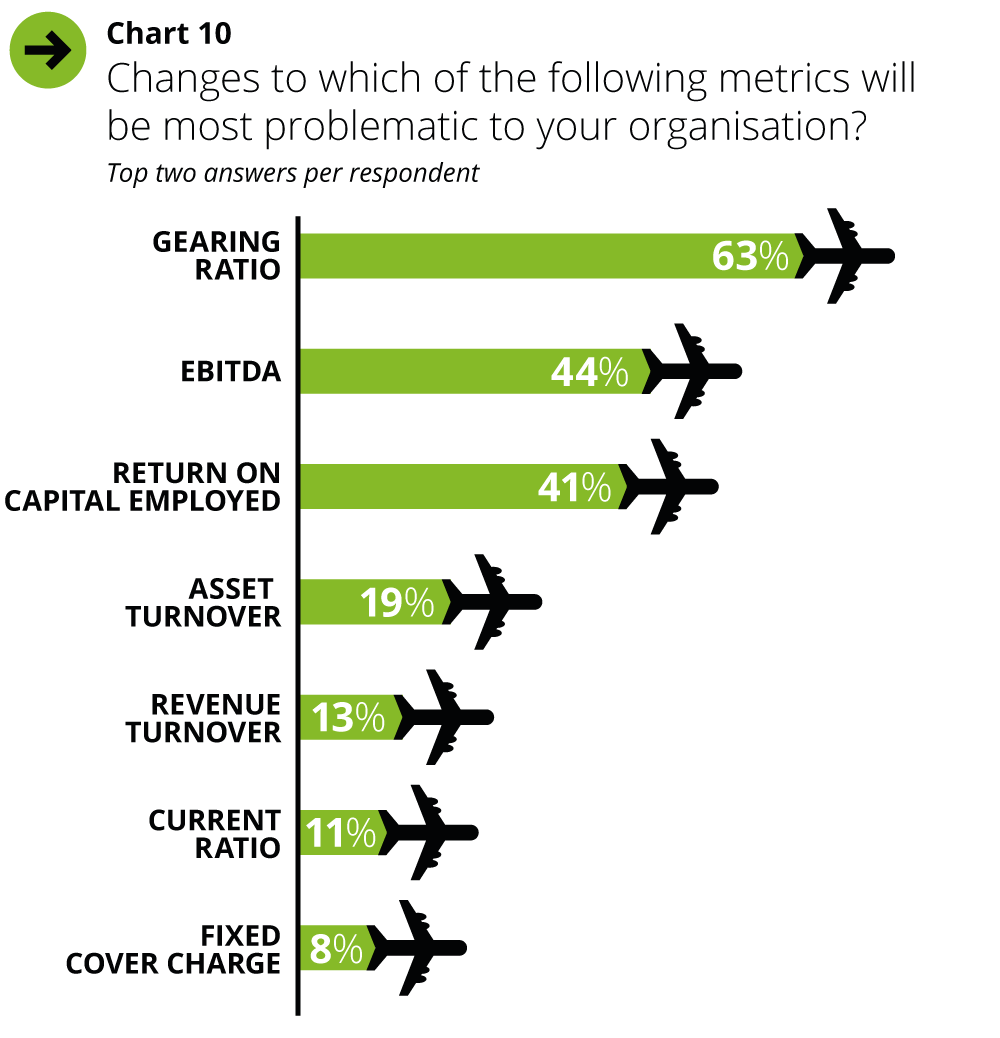

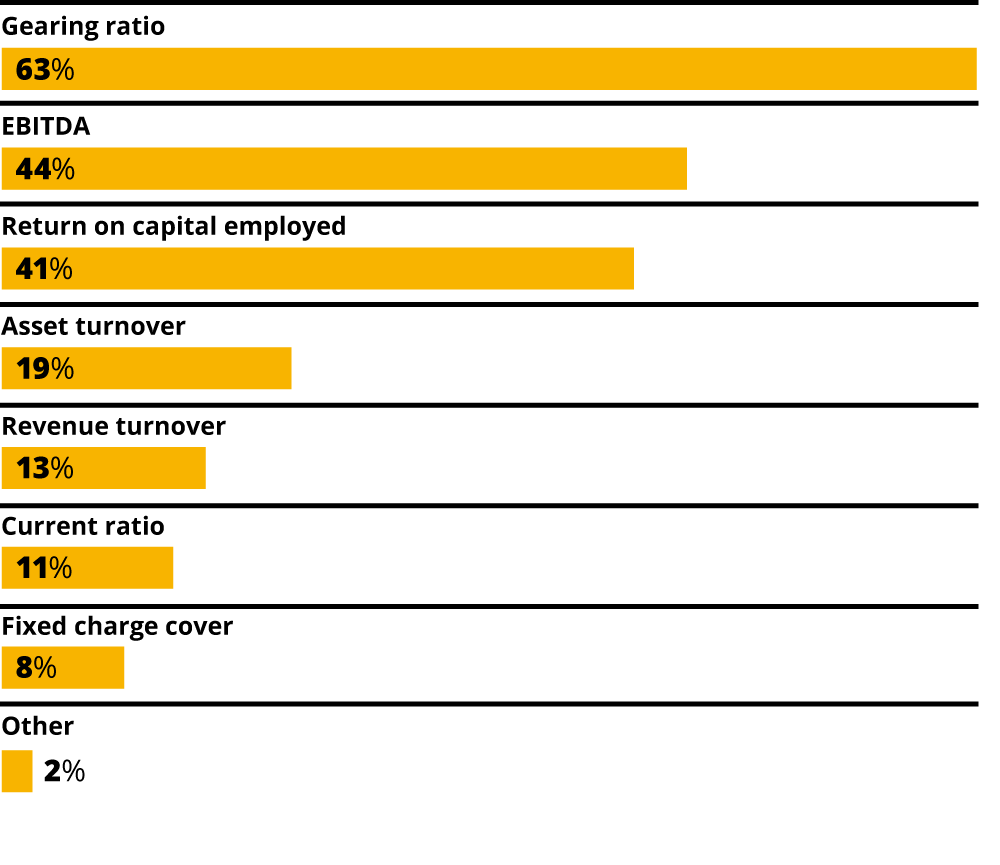

Our survey highlighted seven key financial metrics that would be affected by IFRS 16 (chart 10).

Of these, 63% of respondents and 69% of airlines identify changes to gearing ratios as most problematic. Since IFRS 16 increases the liabilities of any airline with aircraft under operating lease, gearing ratios are set to increase.

“That will have an effect potentially on some financial covenants,” comments Stellwagen CEO Bourgade. He adds that while debt covenants often already account for leases, finance departments will need to ensure this is the case.

Lease data must also be reviewed, a task that 74% of airlines identify as either significantly or moderately challenging.

It could be worthwhile, though. For airlines with few years to run on their leases, their IFRS 16 debt might be lower than adjusted estimates. Air France-KLM, for instance, notified investors in late 2017 that its debt reported under IFRS 16 would be at least €1.5 billion ($1.7 billion) less than previous adjusted estimates.

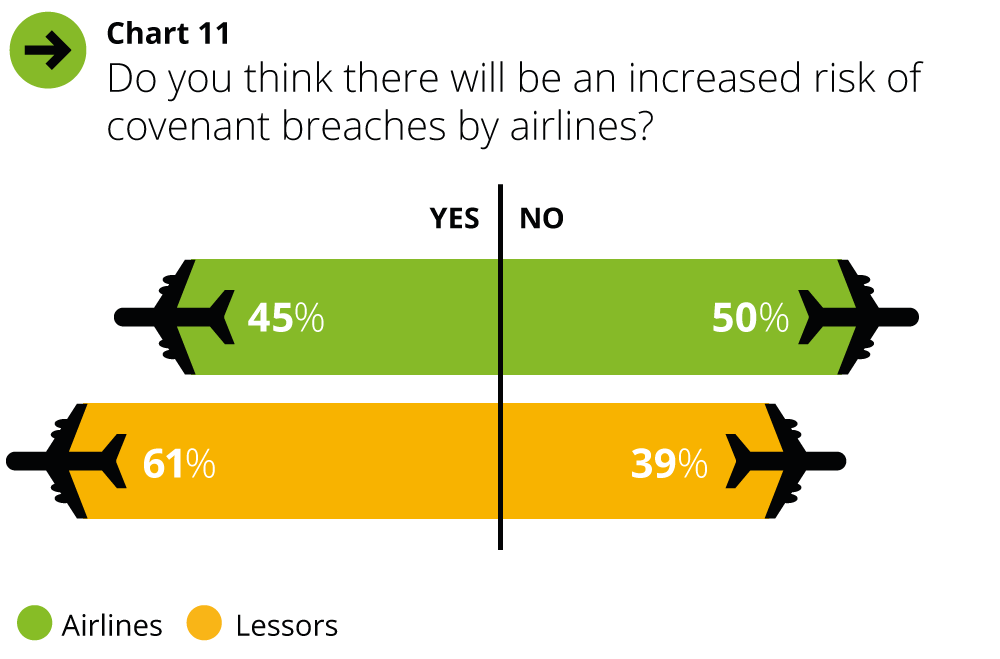

Covenant breaches

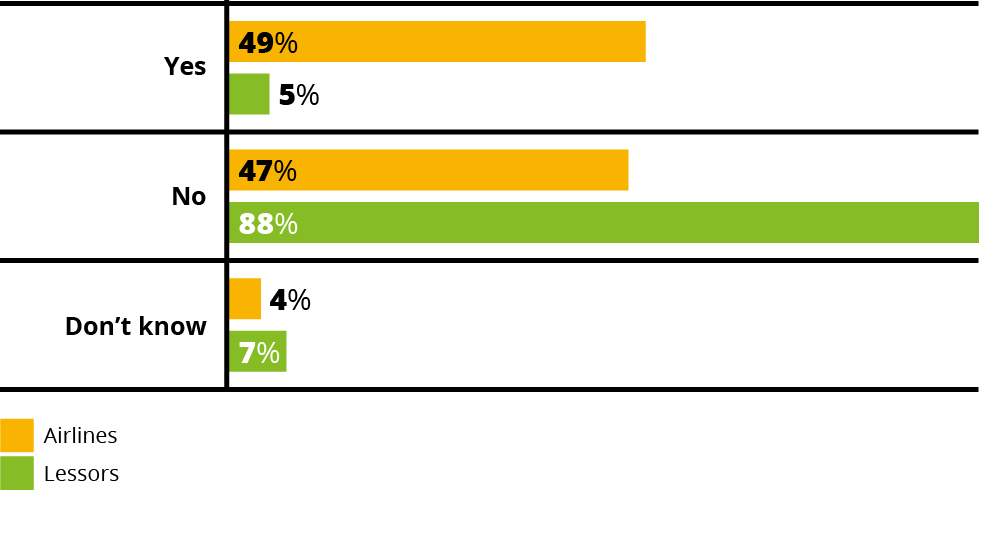

Although operating leases rarely contain covenants pertaining to balance sheet metrics, loan contracts often do. Most lessors (61%) think IFRS 16 means airlines are more likely to breach such covenants, although airlines themselves are more confident they can avoid such violations (chart 11).

Still, while the risk of covenant breaches may be low, proving so will be a laborious job.

“Airlines will have to review all existing loan documentation to make sure that there is not one covenant that has an impact. Maybe they will discover nothing, but they will have to review to check so that will be time-consuming for airlines,” says Bourgade.

Air France-KLM says only its credit facility has covenants that relate to debt levels, and these are already adjusted to include 7x annual aircraft operating lease expense – a common multiplier used by analysts.

“We have agreed with the banks not to change the covenants despite the implementation of IFRS 16,” says de Peslouan at Air France-KLM.

Earnings

IFRS 16 will hit airline debt metrics, but it is also expected to boost parts of the income statements, as rental payments morph into finance costs and depreciation.

Without rental expenses, KPIs such as EBITDA and EBIT will rise, something that airlines and industry identify as the second-most problematic of IFRS 16’s changes to metrics.

De Peslouan, however, thinks that income statement changes will enhance Air France-KLM’s standing in relation to its peers.

“Lufthansa has nearly no operating leases so when we compare Air France-KLM with Lufthansa our operating income and margin are lowered by the operating leases we have.”

She adds that while analysts already include operating leases in their debt analysis, many fail to do the same when comparing KPIs such as EBITDA.

Also relevant is the ‘frontloading’ effect of IFRS 16 accounting, whereby lease expenses are recognised as higher in the early years of a lease. When IFRS 16 is implemented, therefore, airlines with many years to run on most of their leases will experience a greater initial impact on various metrics than those with varied tenors on their balance sheets.

Implementation

“We have noted from our discussions with airlines the cost and effort of implementing and complying with IFRS 16,” says Natixis' aviation finance expert Woon.

Since IFRS 16 makes only minor changes to lessor accounting, airlines bear most of the burden of implementing the new standard. Investors and lessors must ensure their staff can understand changes to lessees’ books, of course, but only a small minority find this a serious challenge.

Most airlines must implement IFRS 16 from 1 January 2019, and even though the implementation date has been known for almost two years, one in every five airlines is uncomfortable about meeting the deadline.

It is also worth noting that 20% of airlines don’t plan any changes to their reporting, a reflection of the fact that IFRS 16 – despite its intention to harmonise lease accounting – is not universally applicable.

Séverine Guffroy, VP Accounting, Air France-KLM and Chairwoman, IATA Accounting Working Group

The US, for instance, will not adopt IFRS 16. Its related standard – ASC 842 – also puts operating leases onto the balance sheet, but doesn’t significantly change P&L reporting.

“Presentation of the income and cash-flow statement will not be the same at all,” says Air France-KLM VP Guffroy.

“If we want to compare Air France-KLM with Delta – one of our biggest partners – it will not be possible without a restatement of the accounts of Delta or of Air France-KLM,” she adds.

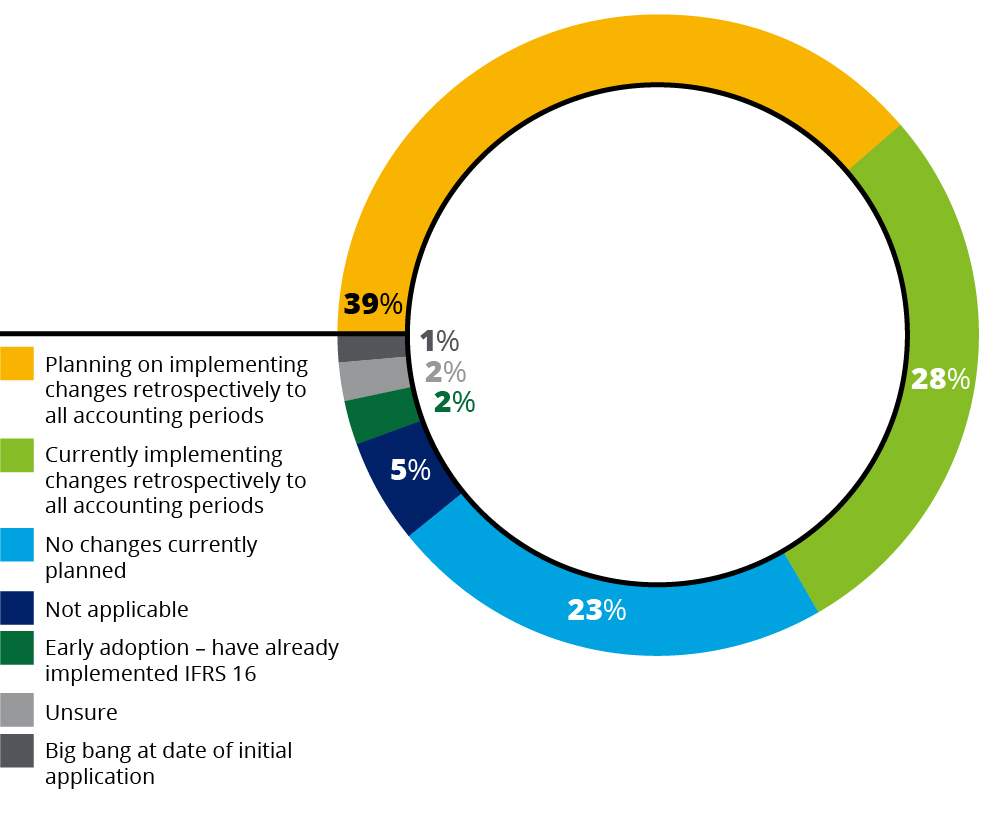

Adoption methodology

Although IFRS 16 contains measures for early adoption, only a handful of airlines are taking that path. Air France-KLM is one, and plans to report in accordance with IFRS 16 from January 2018.

Overall, 75% of airlines in our survey are either planning to, or are currently implementing retrospective changes to past accounting periods (chart 12).

Another way to adopt IFRS 16 is to apply the standard only to accounts from 2019 onwards. This ‘big bang’ approach is much cheaper and simpler than retrospective alterations, but hugely complicates the comparison of pre- and post-2019 accounts. As a result, perhaps, almost no airlines in our survey are considering it.

However, full retrospective transition to IFRS 16 is a huge task that requires the identification, analysis and restatement of contracts that may be many years old, in order to provide meaningful comparisons with previous accounting periods.

About half of airlines across all sizes describe the assessment of current lease data as a moderate challenge, while 25% consider it a significant challenge. Guffroy says that Air France-KLM has identified at least 3,000 contracts that are in the scope of IFRS 16.

Norwegian is going through a similar assessment process, says Østby.

“We’re identifying all contract categories that might be in scope of the standard and determining whether separate contracts also fall within scope.

“We’re also calculating the financial effects of contracts that are within scope and considering how we will implement and present the resulting financial items in our financial reporting.”

Airlines that more heavily rely on leasing are also more likely to be on top of things regarding IFRS 16, the survey indicates.

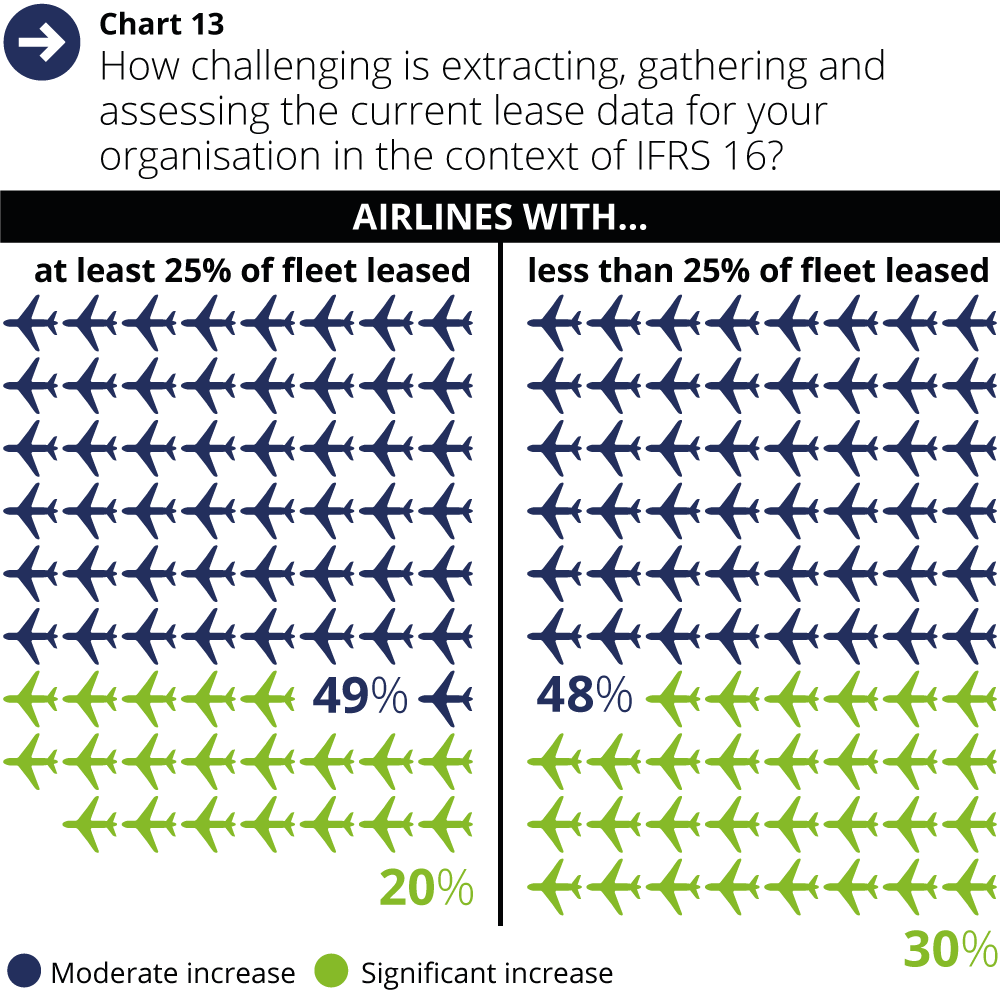

Only 20% of airlines leasing at least a quarter of their fleet say collecting and assessing current lease data is “very challenging,” but almost a third of those with smaller proportions of leased aircraft say so (chart 13).

However, that situation is reversed when it comes to the increased disclosure requirements of IFRS 16. Some 36% of lease-friendly airlines find these very challenging, versus 20% of airlines that lease less than a quarter of their aircraft.

IT readiness

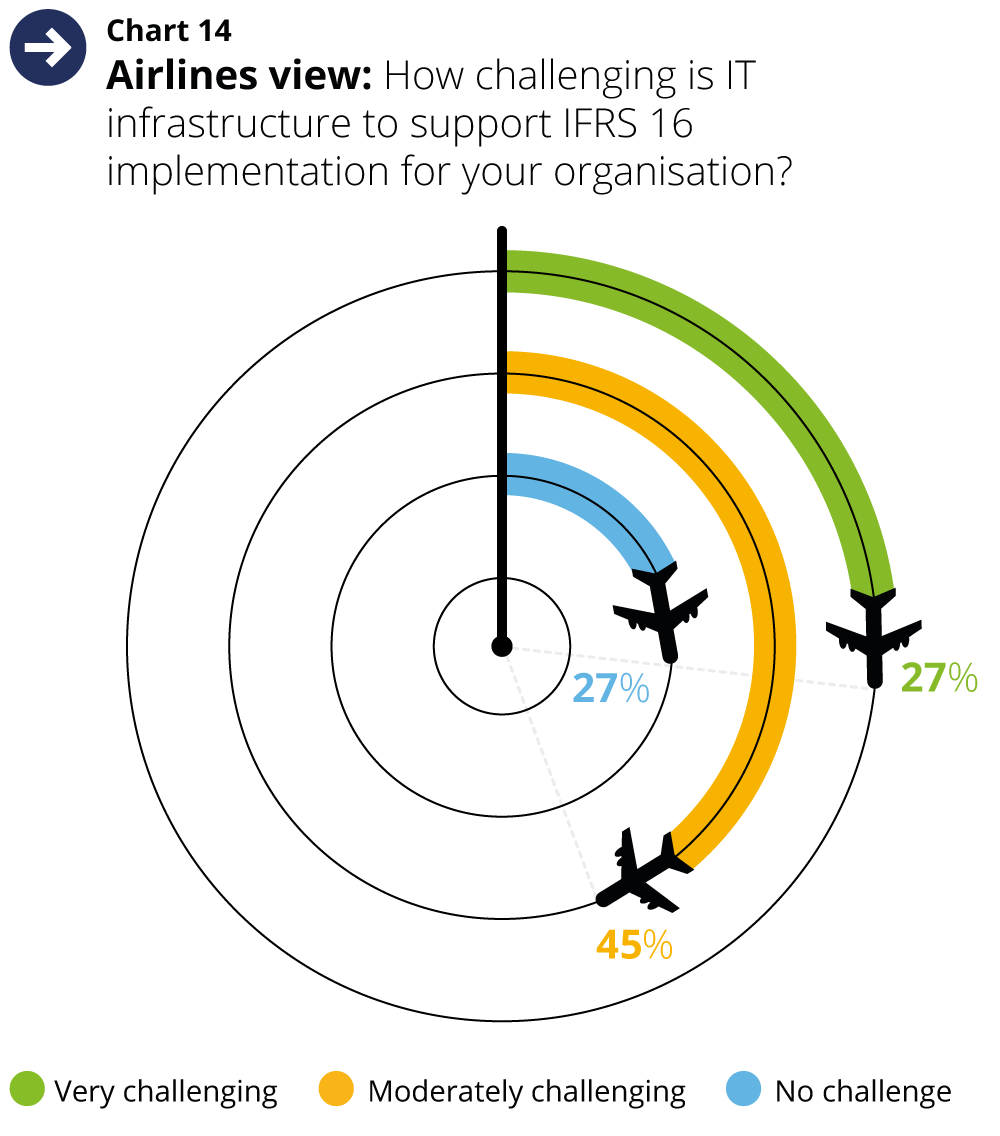

Moving operating leases onto the balance sheet, and then accounting for the resulting depreciation and interest expenses, is an undertaking that stretches the capabilities of simple spreadsheets. IT infrastructure to support the implementation of IFRS 16 poses a challenge for 72% of airlines (chart 14).

In particular, airlines with large leased fleets might need more specialised software. Guffroy says Air France-KLM is the launch customer for new software from SAP designed to manage the accounting treatment under IFRS 16.

“The implementation of the IT tool is a challenge by itself, especially when you are the first to go with it,” she notes.

Only 15% of airlines that lease more than a quarter of their aircraft say they will use spreadsheets for IFRS 16 accounting; that share is almost twice as high for airlines with less than a quarter leased.

Norwegian is among those airlines still evaluating its options, says Østby.

“Some operators develop solutions to cover the requirements of IFRS 16, which we are considering. We’re also seeing how one or more of our existing systems can cover the needs of IFRS 16.

“In addition, we are assessing which functionality our lease administration system can offer but we must see how the systems, required by IFRS 16, can combine specialty needs in their processes.”

Conclusion

Implementation of IFRS 16 is clearly a huge task for airline accountants. The new standard makes profound changes across balance sheets and income statements, all of which must be carefully applied and explained to investors.

While disclosure and communication requirements are significant, airlines’ preference to apply IFRS 16 retrospectively only heightens the workload. Larger carriers will have to find and analyse thousands of old contracts, a job that may force them to beef up financial departments or recruit outside help.

Airlines in our survey indicate they are ready for the challenge, as do lessors and investors, which must adapt their analysis of airline financials. Less clear is if they know what comes next.

For instance, lessors and airlines interviewed for this report don’t expect IFRS 16 to alter lease contracts, but most of our more than 380 survey respondents think otherwise.

Some uncertainty about future leasing activity remains. In interviews, lessors appear sure that the commercial advantages of operating leasing will override any concerns about its accounting treatment. That anecdotal confidence is reflected by the survey, to the extent that a small majority of respondents expect leasing and sale-leaseback volumes to stay the same or even to increase.

Financiers, meanwhile, say IFRS 16 is unlikely to influence them, since they already capitalise operating leases.

Sometimes, though, their adjustments do not extend across all of an airline’s key metrics. Even where they do, there is potential for IFRS 16 figures to diverge significantly from adjusted estimates.

Only a tiny fraction of survey respondents thinks IFRS 16 is a bad idea. Instead, most applaud the intent to harmonise lease accounting, even though the standard is not universally applicable. Certainly, IFRS 16 will facilitate comparison of airlines in, say, Europe, but it may complicate peer analysis if an airline has not adopted IFRS, as will be the case in the US.

Airlines, lessors and investors must tackle the nuances of IFRS 16 to negotiate this new accounting landscape. By doing so they can better appreciate any commercial consequences of the new standard, and adjust their operations accordingly.

About /

Appendix

For this report, Euromoney Institutional Investor Thought Leadership surveyed 381 senior executives from the aviation finance industry. 41% or respondents hold C-level positions in their companies, a further 30% are vice presidents and senior directors. The others are senior managers in a variety of roles including regulatory, finance, legal and compliance.

54% of respondents work for airlines and lessors. 20% are working for investors or the financial services industry to aviation finance. The remainder includes predominantly non-financial advisers, for instance from the legal community.

37% of respondents are based in Europe, Middle East and Africa, 32% in Asia-Pacific, and 31% in the Americas.

In addition to the survey, in-depth interviews were conducted with nine senior industry executives and financiers.

The survey was conducted during the period 10 October to 3 November 2017. In-depth interviews took place throughout October and November 2017.

Balancing the Books: IFRS 16 and Aviation Finance is a Euromoney Institutional Investor Thought Leadership report, prepared in conjunction with Deloitte. The research was conducted by Euromoney Institutional Investor Thought Leadership.

This content is made available for your general information and is not intended to address your particular requirements and may include inaccuracies or typographical errors. The content does not constitute any form of advice, recommendation or arrangement by us and is not intended to be relied upon by users in making (or refraining from making) any specific investment or other decisions. Neither Deloitte nor any member firm of Deloitte Touche Tohmatsu Limited, Euromoney Institutional Investor PLC or their related entities make any representations or warranties and, to the fullest extent allowed by law, exclude all implied warranties regarding the suitability of the information; or the accuracy, availability, reliability, completeness of the content.

What level of impact will the adoption of IFRS 16 have on your business?

Do you feel you have a comprehensive understanding of the incoming IFRS 16 standard and how it differs from current accounting standards?

How challenging are the following issues for your organisation in the context of IFRS 16?

IFRS 16 eliminates nearly all off balance sheet accounting for lessees and will impact many companies’ financial metrics. Changes to which of the following metrics will be most problematic to your organisation? (select two)

Do you have the required IT infrastructure in place to deal with the adoption of IFRS 16?***

* Respondents working for airlines only

Will the number of the following types of aircraft transactions across markets change in light of IFRS 16?

To minimise the impact of IFRS 16 existing leases will be renegotiated and standard terms for new leases will change.

What aspects of existing leases/new standard leases do you expect to change in light of IFRS 16? (select all that apply)*

* Respondents “strongly agreeing” or “agreeing” with question 7 only

How will IFRS 16 impact the cost of financing/funding of airlines/lessors?

How will IFRS 16 impact the sources of financing/funding of airlines/lessors?

Do you think there will be an increased risk of covenant breaches by airlines/lessors?

IFRS 16 will become effective as of 1 January 2019. Do you consider this timeframe sufficient for your company to make the necessary arrangements?

What stage is your company at in respect of implementing IFRS 16?

For which stakeholders will IFRS 16 be most positive/most negative?

What is the most important benefit of implementing IFRS 16 for the international aviation finance industry?

From a financial reporting perspective, what will be the most challenging aspect for your business?

Note: Due to rounding, some totals do not equal 100%.

Click the button to download this report as a PDF to take away and share.

Balancing the Books

IFRS 16 and Aviation Finance

Advisory Panel:

Brian O’Callaghan, Lead Audit & Assurance Partner, Aircraft Leasing & Finance, Deloitte

Martina McDevitt, Audit & Assurance Director, Aircraft Leasing & Finance, Deloitte

Mike Duff, Head of Data Products, Airfinance Journal

Managing Editor: Ben Bschor

Writer: Alex Derber

Designer: Claire Boston

About Deloitte

Deloitte is the largest global professional services and consulting network, with approximately 263,900 professionals in more than 150 countries. Deloitte’s dedicated Aircraft Leasing & Finance advisory team delivers first-class advice to some of the largest aircraft lessors in the world and are ready to assist in the fields of tax, audit, corporate finance and consulting. Our people have the leadership capabilities, experience and insight to collaborate with clients so they can move forward with confidence.

About Euromoney Institutional Investor Thought Leadership

Euromoney Institutional Investor Thought Leadership creates thought-provoking content for global business leaders. EIITL's editorial team is hugely experienced in devising memorable, long-lasting and effective content programmes. With a team of independent journalists, experienced editors and professional marketers, we create reports, surveys, blogs, articles, videos, infographics and animations. All of our content is unbiased, original, research driven and audience-led.

About Airfinance Journal

Airfinance Journal is a market leading financial publication of the global aircraft and aviation business. Published since 1979, it has been at the forefront of supporting and informing aviation professionals. The Journal includes the latest news, analysis and data relating to the financing of airlines, aircraft leasing companies and manufacturers.