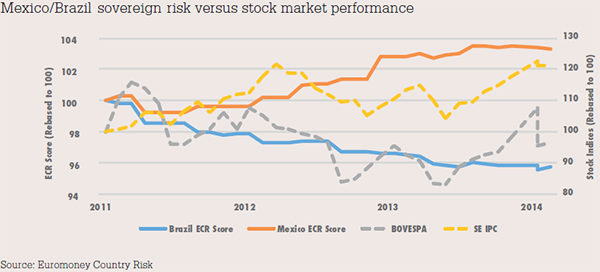

Four years ago, Brazil had one of the world’s most dynamic economies, while low-growth Mexico was shunned by EM investors seeking higher returns elsewhere. Fast forward to 2014, and Mexico is now the poster child of the emerging markets following a series of ground-breaking economic reforms. In Brazil, growth has slowed to a trickle against a backdrop of policy deadlock and a deeply divisive Fifa World Cup. Euromoney Country Risk data illustrate how changing perceptions of the two countries’ risks drove performance of the domestic equity markets.

Brazil and Mexico follow divergent long-term risk trends

October 2014

Investors should take note: LatAm’s big two have been offering contrasting portfolio options for some time. This year is no exception.

Videgaray pulls Mexico into shape

October 2014

Mexico’s government has introduced a swathe of structural reforms that aim to cut key input costs in the economy, arrest deteriorating productivity and improve the country’s long-term growth rates. However, it is the finance minister’s recent energy reforms that have most made economists and investors buoyant about the outlook for Latin America’s second biggest economy.

Economic growth: Two-speed Latin America

September 2014

Mexico’s energy reforms should kick-start growth in its lacklustre economy while Brazil appears to have no strategic planning in place.

Economic policy: Investors try to get a sense of Brazil in 2015

March 2014

Post-election policies still hard to predict; fiscal discipline key to investments.

Mexico’s economy tipped to overtake Brazil’s

August 2012

Strong growth expected from banks; Attractive market for foreign investment